What Is Inheritance Tax?

An inheritance tax (also called “death tax” or estate tax) is a tax levied on the total value of property, assets, and wealth transferred from a deceased person to their heirs.

Key Components of Inheritance Tax

- Tax on the Inheritance Itself: The tax is calculated on the total estate value—including real property, bank accounts, investments, vehicles, jewelry, and business assets—before distribution to heirs.

- Tax Before Distribution: In countries that tax inheritance, the heirs typically pay the tax from the estate before receiving their share.

- Relationship-Based Rates: Many countries adjust inheritance tax rates based on the relationship between deceased and heir (spouses pay less, distant relatives pay more).

- Threshold or Exemption Amount: Most jurisdictions exempt a certain amount of inheritance (called the “exemption threshold” or “nil-rate band”).

Why Governments Impose Inheritance Tax

Governments historically used inheritance tax for two main reasons:

- Revenue Generation: Creating a new source of tax income for public services and infrastructure.

- Wealth Equality: Reducing wealth concentration in the hands of the richest families across generations.

In India’s case: The government tried inheritance tax (Estate Duty) but ultimately found it failed to achieve both goals—we’ll explore why in detail below.

Direct Answer: Is There Inheritance Tax in India?

No, India does NOT have inheritance tax.

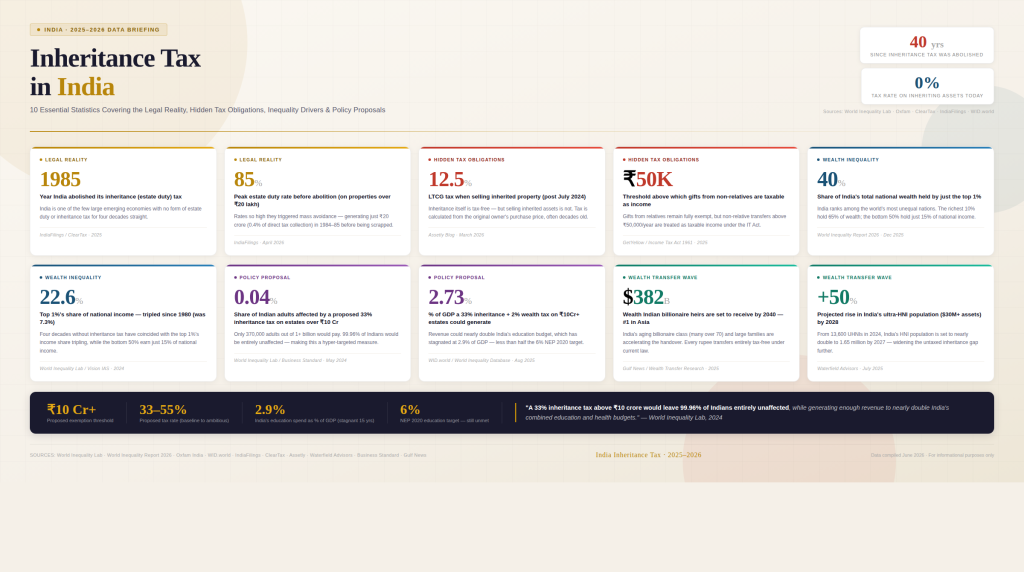

India abolished its inheritance tax system—called Estate Duty—in 1985, more than 40 years ago. This means:

- Zero tax on inherited property

- Zero tax on inherited money or assets

- Zero tax on the transfer of wealth to heirs

- No requirement to pay tax to receive your inheritance

This makes India unique among major economies. While developed nations like the USA, UK, Japan, and Germany impose inheritance taxes, India allows wealth to pass to the next generation tax-free.

However, The Abolition Comes With Important Caveats

Important: Just because there’s no inheritance tax doesn’t mean your inherited assets are completely tax-free. Instead, taxes shift to the income and gains generated from those assets—a distinction critical to understand.

Inheritance Tax History in India: Timeline (1953-2025)

1. 1953: Estate Duty Introduced

What Happened: Post-independence India, under Prime Minister Jawaharlal Nehru, introduced Estate Duty as part of broader economic reforms. The goal: prevent wealth concentration and fund public services.

Tax Rate: Graduated from 0-85% depending on estate value

Why It Was Created: The Indian government was concerned that large family fortunes would accumulate across generations, perpetuating inequality. Taxing the transfer of wealth at death seemed like an ideal solution.

2. 1963: Estate Duty Rates Increased

What Happened: Maximum tax rate pushed to 85% on the largest estates.

The Idea: Higher taxes on ultra-wealthy families would fund social programs and education.

Reality: Wealthy families began exploring loopholes.

3. 1975: Capital Transfer Tax Replaces Estate Duty

What Happened: Government replaced Estate Duty with a new “Capital Transfer Tax,” modeled after the UK system, to close loopholes.

Why the Change: Estate Duty had too many exemptions and wasn’t generating expected revenue.

4. 1985: Estate Duty and Capital Transfer Tax Abolished

What Happened: After 30+ years of trial, the Finance Minister under the Rajiv Gandhi government decided to completely abolish estate duty and capital transfer tax.

Why This Happened: The government concluded the taxes had failed on all counts (detailed below).

Impact: Overnight, India moved from having one of the world’s highest inheritance taxes (85%) to zero.

5. 2015: Wealth Tax Also Abolished

What Happened: India also abolished Wealth Tax in 2015—a direct tax on total wealth (separate from inheritance).

Current Status: India has had zero inheritance tax for 40+ years and zero wealth tax for 10+ years.

Why Was Inheritance Tax Abolished in India? (3 Critical Reasons)

Understanding why India abandoned inheritance tax is crucial—it shows the tax was fundamentally flawed despite good intentions.

Reason #1: Minimal Revenue Generation (Tax Efficiency Failure)

The Problem: Estate Duty generated shockingly little revenue despite high tax rates.

The Numbers:

- In 1985 (final year of operation), Estate Duty contributed only 0.4% of total direct tax collection

- This came from taxing some of the largest wealth transfers in the country

- The marginal return was not worth the administrative burden

The Irony: The tax cost more to collect than it generated.

- IRS estimates suggested it cost ₹2-3 to collect every ₹1 of inheritance tax revenue

- The tax offices had to hire specialized valuers, assess properties, and defend valuations in court

- The result: Administrative expenses exceeded actual tax collected

Finance Minister’s Statement (1985): “The inheritance tax regime has consistently failed to serve its stated purpose of generating significant public revenue. The tax-to-administrative-cost ratio makes this an inefficient instrument of policy.” — V.P. Singh, Finance Minister under Rajiv Gandhi

Reason #2: Impossible to Administer (Valuation Complexity)

The Core Problem: How do you fairly value assets that don’t have a market price?

Specific Challenges:

- Family Business Valuation

- What’s a 50-year-old family manufacturing business worth?

- Who decides: the tax office or the family?

- Disputes often lasted 5-10 years in litigation

- Agricultural Land Valuation

- Agricultural land in different regions has vastly different values

- Should fertile land in Punjab be valued differently from land in Rajasthan?

- Who determines the “fair market value”?

- Intellectual Property & Goodwill

- What’s the value of a brand name or business reputation?

- These are transferred at death but hard to quantify

- Ancestral Property Without Recent Transactions

- If a property hadn’t been sold in 30 years, what was its “value”?

- Tax authorities and families constantly disputed valuations

Result: Endless litigation and appeals, consuming judicial resources.

Reason #3: Widespread Tax Evasion (Behavioral Distortion)

The Unintended Consequence: High inheritance tax rates encouraged people to break the law or move assets abroad.

What Happened:

- Capital Flight (Asset Exodus)

- Wealthy families moved businesses and assets to countries without inheritance tax

- Family businesses established in Singapore, Hong Kong, or the US to avoid Indian death taxes

- Loss of business, employment, and tax base for India

- Benami Transactions (Hidden Ownership)

- Property held in “benami” (concealed names) to hide true ownership from tax authorities

- Spouses, relatives, or third parties held assets nominally

- When the true owner died, the property was already in another name—no inheritance tax!

- Trust Structures & Loopholes

- Wealthy families used trusts and complex structures to transfer wealth during lifetime, avoiding death-time taxation

- Tax authorities spent years trying to close loopholes

- Underreporting & Documentation Issues

- Families underreported asset values

- Incomplete documentation made it impossible for tax authorities to assess fairly

The Bottom Line: Those wealthy enough to afford expert advice easily avoided the tax. Those who couldn’t afford advice (middle-class families) bore the burden.

Global Context: Inheritance Tax Rates Around the World

To understand why India’s decision matters, here’s how India compares to other major economies:

| Country | Tax Rate | Exemption Threshold | Year Abolished/Started |

|---|---|---|---|

| Japan | Up to 55% | ¥30 million (~₹1.6 Cr) | Still in effect |

| France | Up to 60% | €100,000 (~₹82 lakh) | Still in effect |

| Germany | Up to 30% | €75,000-€400,000 (~₹61-₹33 lakh) | Still in effect |

| UK | 40% | £325,000 (~₹3.7 Cr) | Still in effect |

| USA | Up to 40% (Federal) | $13.61 million (~₹110 Cr) | Still in effect |

| Canada | 0% (on inheritance) | N/A | Never taxed |

| **INDIA | 0% | N/A | Abolished 1985 |

| Australia | 0% | N/A | Abolished 1979 |

| South Korea | Up to 50% | Varies | Still in effect |

| China | 0% (Not implemented) | Proposed | Never implemented |

Key Insights

India’s Unique Position:

- Among major Asian economies, India is the ONLY one without inheritance tax

- This gives Indian families a massive wealth transfer advantage compared to Japan, South Korea, or developed nations

Why Developed Nations Keep It:

- They have broader exemption thresholds (e.g., USA exempts $13.61 million)

- Only ultra-wealthy families pay; middle-class inheritance is exempt

- Revenue generation is significant due to large wealth transfers

Why India Abandoned It:

- Threshold was too low (everyone paid)

- Revenue was minimal despite high rates

- Administration was impossible

- Behavioral distortion (evasion) was rampant

Context for Wealth Inequality

Here’s why inheritance tax matters for the wealth conversation:

India’s Wealth Concentration is Significant:

- 58% of India’s total wealth belongs to the wealthiest 1% of the population

- This is higher than the global average of 40-45%

- In developed nations with inheritance tax, this gap is slightly smaller due to generational wealth erosion through taxation

The Trade-off India Made: Rather than taxing inheritance and facing all the problems above, India chose to:

- Allow wealth to transfer freely (zero inheritance tax)

- Tax the income generated from inherited assets instead

This approach has worked reasonably well in practice—it’s simpler, more enforceable, and less evasion-prone.

What Taxes STILL Apply to Inherited Assets in India?

Here’s the critical point many people misunderstand: No inheritance tax doesn’t mean inherited assets are completely tax-free.

Instead, you pay tax on:

Gifts (in some cases, if inheriting through a gift rather than succession)

Income from inherited assets

Gains when you sell inherited assets

TAX #1: Income Tax on Income From Inherited Assets

When you inherit an asset that generates income, that income becomes YOUR taxable income.

Examples:

- Inherited Rental Property

- Your father owned a residential property that generated ₹50,000/month in rent

- After his death, you inherit the property and receive the rent

- That ₹50,000/month is now YOUR rental income—fully taxable at your income tax slab

- You must file ITR and report this income

- Inherited Bank Deposits & Interest

- Father had a bank fixed deposit with ₹20 lakhs earning 6% annually

- You inherit the FD; the annual interest of ₹1.2 lakhs is YOUR income

- Taxable as “Income from Other Sources” at your slab rate (5%, 20%, or 30%)

- Inherited Dividend-Yielding Investments

- Father owned mutual funds/stocks earning ₹5 lakhs/year in dividends

- You inherit these; the dividend income is YOUR income

- Taxed as “Income from Other Sources”

- Inherited Life Insurance (Maturity/Claim)

- Father’s life insurance policy matures after his death with a payout of ₹50 lakhs

- You receive ₹50 lakhs as beneficiary

- The insurance payout itself is usually tax-free, BUT any bonus component may be taxable to the deceased’s estate

Tax Rate: Your income tax slab (5%, 20%, or 30% depending on total income + surcharge + cess)

TAX #2: Capital Gains Tax When You Sell Inherited Assets

This is the biggest tax implication most people face. When you sell inherited property or investments, you pay capital gains tax.

Key Advantage: Step-Up in Basis

India provides a valuable benefit: The cost of acquisition “steps up” to the asset’s value on the date of death, not the original purchase price.

Example to Illustrate:

Without Step-Up (If it applied):

- Father bought property in 2005 for ₹10 lakhs

- Asset appreciates to ₹1 crore by 2024 (when father dies)

- If you had to use father’s original cost (₹10 lakhs) for capital gains calculation, your gain would be ₹90 lakhs—huge!

- Tax on ₹90 lakh gain: ~₹18 lakhs (20% with indexation)

With Step-Up (What Actually Happens in India):

- Father bought property in 2005 for ₹10 lakhs

- Asset appreciates to ₹1 crore by 2024 (when father dies)

- Your cost of acquisition is ₹1 crore (the FMV on date of death)

- If you immediately sell for ₹1 crore, gain = ₹0

- Tax = ₹0

This step-up benefit is HUGE for inherited assets.

Calculating Capital Gains Tax on Inherited Property: Step-by-Step Guide

When you sell inherited property, here’s exactly how to calculate capital gains tax:

STEP 1: Determine the Cost of Acquisition (COA)

The Cost of Acquisition is the Fair Market Value (FMV) of the asset on the date of death of the original owner.

- This is NOT the original purchase price

- This is NOT the value you paid (you didn’t pay anything—you inherited it)

- This is the market value on the specific day the person died

How to Determine FMV:

- For Real Property: Get a valuation certificate from a registered valuer or bank

- For Shares: NSE/BSE closing price on the date of death

- For Mutual Funds: NAV on the date of death

- For Bank Accounts: The balance on the date of death

STEP 2: Determine the Holding Period

Holding period includes the time the ORIGINAL OWNER held the asset, plus your time as the heir.

Rule:

- If total holding period (original owner + you) > 24 months = Long-Term Capital Gains (LTCG)

- If total holding period ≤ 24 months = Short-Term Capital Gains (STCG)

Important: You don’t get to “reset” the clock when you inherit. The original owner’s holding period counts.

Example:

- Father bought property on Jan 1, 2003

- Father died and you inherited on June 1, 2019 (you’ve now held it for 6 months)

- You sell on March 30, 2025

- Total holding period: Jan 2003 → March 2025 = 22+ years

- Classification: LTCG ✓

STEP 3: Calculate the Capital Gain

Capital Gain = Sale Price – Indexed Cost of Acquisition

For LTCG, the cost of acquisition is adjusted for inflation using the Cost Inflation Index (CII).

Formula:

Indexed COA = Original COA × (CII of Year of Sale / CII of Year of Death)

Capital Gain = Sale Price − Indexed COAWhat is CII? The Cost Inflation Index is released by the Income Tax Department annually. It reflects inflation and is used to adjust the cost basis of long-term assets.

CII Values (Select Years):

2001-02: 100

2005-06: 113

2010-11: 167

2015-16: 254

2019-20: 289

2020-21: 301

2021-22: 317

2022-23: 331

2023-24: 348

2024-25: 365 (approx.)STEP 4: Apply the Correct Tax Rate

For Long-Term Capital Gains (> 24 months holding):

- Tax rate: 20% with Cost Inflation Index benefit (standard)

- OR 12.5% without indexation (rarely applicable)

- Add: 4% health and education cess on the tax

- Add: Applicable surcharge (15%-37% depending on total income)

Tax = 20% × Capital Gain + Cess + Surcharge

For Short-Term Capital Gains (≤ 24 months holding):

Add: Cess + surcharge as applicable

Taxed as regular income at your income slab

Can be 5%, 20%, or 30% depending on your total income (including the gain)

Worked Example: Real Numbers For Inherited Property Tax Calculation

Let me walk you through a realistic scenario with actual numbers:

Scenario: Rahul Inherits His Father’s Apartment

The Facts:

- Father’s Purchase: January 1, 2005

- Original Purchase Price: ₹20,00,000

- Father’s Death: June 15, 2023

- FMV on Date of Death: ₹1,00,00,000 (₹1 crore)

- Rahul Sells: March 20, 2025

- Sale Price: ₹1,20,00,000 (₹1.2 crore)

- Rahul’s Income Slab: 30% (High earner)

Calculation:

STEP 1: Cost of Acquisition

- COA (FMV on date of death) = ₹1,00,00,000

STEP 2: Holding Period

- January 2005 → March 2025 = 20+ years

- Classification: LTCG ✓

STEP 3: Capital Gain (With Indexation)

- CII (June 2023): 342 (approximate)

- CII (March 2025): 365 (approximate)

- Indexed COA = ₹1,00,00,000 × (365/342) = ₹1,06,72,514

- Capital Gain = ₹1,20,00,000 – ₹1,06,72,514 = ₹13,27,486

STEP 4: Calculate Tax

- LTCG Tax (20%) = ₹13,27,486 × 20% = ₹2,65,497

- Add Health & Education Cess (4%) = ₹2,65,497 × 4% = ₹10,620

- Surcharge (for 30% slab): 15% of ₹2,65,497 = ₹39,825

- Total Tax = ₹2,65,497 + ₹10,620 + ₹39,825 = ₹3,15,942

Net Result:

Sale Price: ₹1,20,00,000

Less: Tax Liability: -₹3,15,942

Amount Rahul Keeps: ₹1,16,84,058

Effective Tax Rate: 2.63% (very low due to indexation benefit)Key Insight: Due to indexation benefit, Rahul keeps 97.37% of the sale price despite India’s capital gains tax. The inflation adjustment significantly reduces the taxable gain.

Tax Optimization Strategies for Inherited Assets

Now that you understand how inheritance tax works (or doesn’t), here are strategies to minimize taxes when dealing with inherited assets:

Strategy #1: Use Section 54 Exemption (Residential Property)

What It Is: If you inherit a residential property and sell it, you can invest the gains into ANOTHER residential property and claim a tax exemption.

Conditions:

- The property you inherited must be residential

- You must reinvest the entire sale proceeds in another residential property

- The new property must be purchased within 2 years of the sale (or 1 year before)

Tax Benefit: 100% exemption on capital gains (No capital gains tax!)

Example:

- You sell inherited apartment for ₹1.2 crore

- Capital gain = ₹20 lakhs

- You buy another apartment for ₹1.2 crore within 2 years

- Capital gains tax = ₹0 (completely exempt under Section 54)

When to Use: If you want to upgrade your residential property or move to a different city but keep a residential property.

Strategy #2: Use Section 54EC Bond (Any Asset Type)

What It Is: You can invest up to ₹50 lakh per financial year in specific government securities under Section 54EC to defer capital gains tax.

Conditions:

- You must invest within 6 months of selling the inherited asset

- Maximum investment: ₹50 lakh per FY

- Investment period: Minimum 5 years

Tax Benefit: 100% exemption on capital gains up to ₹50 lakh

Example:

- You sell inherited property for ₹1 crore

- Capital gain = ₹30 lakh

- Invest ₹30 lakh in Section 54EC bonds

- Capital gains tax = ₹0 (completely exempt)

When to Use: When you don’t have another residential property to buy but want to defer/avoid capital gains tax.

Strategy #3: Timing the Sale (Utilize LTCG Benefit)

Key Insight: LTCG tax (20% with indexation) is lower than STCG tax (your income slab rate, could be 30%).

Action: If you inherited an asset with less than 24 months of holding (original owner + you), wait until the 24-month mark to sell.

Example:

- You inherit property on June 1, 2023 (original owner had it since March 2019 = 39 months)

- Total holding = 39 + time since inheritance

- Any sale after June 1, 2025 (24 months) = LTCG rate (20%)

- Sale before June 1, 2025 = STCG rate (30% if you’re in highest slab)

- Tax savings by waiting 6 months: 10% of capital gain

Strategy #4: Gift Inherited Property (If Beneficiary Can Use Section 54)

Complex but powerful: If you inherit property but know you won’t be the one using it for the long term, consider GIFTING it to a family member who will use it under Section 54.

Why: When they eventually sell under Section 54, they get exemption you couldn’t claim.

Consult a Tax Consultant: This requires detailed planning based on your specific situation.

Strategy #5: Document Everything and Update Cost Records

Simple but Critical:

- Get a Valuation Certificate from a registered independent valuer showing FMV on date of death

- Keep this along with the will, death certificate, and inheritance documents

- Update property records to show the date of death valuation as the new cost basis

- When selling 3-5 years later, you’ll have exact documentation for the tax authority

Tax Consultant Benefit: A tax consultant can help you determine the accurate FMV, file necessary forms, and ensure your cost records are CII-adjusted correctly.

Inheritance Tax Treatment for Specific Asset Types

Different inherited assets have different tax rules. Here’s a breakdown:

1. Inherited Real Property (Land & Buildings)

What Happens:

- No inheritance tax on receiving it

- Rental income (if any) = Your taxable income

- Capital gains tax when you sell (as detailed above)

Optimization: Use Section 54 exemption if applicable

Key Document: Valuation certificate from registered valuer

2. Inherited Bank Accounts & Fixed Deposits

What Happens:

- No inheritance tax on the balance

- Interest earned on FD/savings = Your taxable income

- No capital gains (bank deposits don’t appreciate)

If FD is in Father’s Name Still:

- Interest earned up to date of death belongs to the deceased’s estate (taxed in deceased’s last ITR)

- Interest earned after = Your income

Tax Impact: Minimal if only principal is inherited; interest earned thereafter is taxable

3. Inherited Life Insurance

What Happens:

- Maturity/Death Benefit: Generally tax-free to the policyholder or beneficiary

- Exceptions:

- If policy transferred as gift during lifetime, some rules apply

- Loans against insurance are not taxable

No capital gains on insurance payout (it’s not considered a capital asset)

Best Case: Life insurance is essentially inheritance-tax-free and income-tax-free

4. Inherited Shares & Mutual Funds

What Happens:

- No inheritance tax on receiving shares

- Dividend Income: Your taxable income (if dividends are paid)

- Capital Gains: Taxed when you sell shares/units

Holding Period: Includes original owner’s holding period

- If original owner held >1 year = Equity shares have LTCG benefit

- If original owner held <1 year = STCG (your slab rate)

For Mutual Funds:

Debt MF held >3 years = LTCG (20% with indexation)

Equity MF held >1 year by original owner = LTCG (20% with indexation)

5. Inherited Vehicles

What Happens:

- No inheritance tax

- No income tax (vehicles don’t generate income)

- Capital Gains: Technically applies if you sell at a profit, but almost never assessed

Practical Impact: Vehicles are treated as consumable assets; no capital gains tax usually applies

6. Inherited Jewelry & Gold

What Happens:

- No inheritance tax

- If you sell for profit: Capital gains tax applies

- Difficult to prove cost basis (historical purchase)

Practical Challenge: Hard to document original cost; most assessors don’t pursue jewelry cases

7. Inherited Family Business or Partnership

What Happens:

- No inheritance tax

- Business income continues to be taxable (to whoever runs it)

- If you sell the business: Capital gains tax applies

- Complex valuation issues

Important: Consult a tax consultant specializing in business succession for detailed planning

Special Case: NRIs Inheriting Indian Property

NRI Definition

An NRI (Non-Resident Indian) is an Indian citizen who:

- Lives outside India for more than 182 days in a financial year, or

- Earns income outside India for most of the year

Special Rules for NRIs:

1. CAN NRIs Inherit Indian Property?

- ✓ Yes, absolutely. NRIs can inherit from parents/relatives in India without restrictions

2. Is Inheritance Tax Applicable for NRIs?

- ✓ No, same as Indians. There’s no inheritance tax in India for anyone—citizens or NRIs

3. What About Income/Gains?

- Income Tax: If NRI earns rental income from inherited Indian property, it’s taxable in India under “Income from House Property” rules

- Capital Gains Tax: When NRI sells inherited Indian property, capital gains tax applies (same rates as Indians)

- TDS: 30% TDS is deducted on rent income from Indian property

4. Special Taxes for NRIs:

- Long-Term Capital Gains: 20% (with indexation, same as Indians)

- Short-Term Capital Gains: 40% (higher than Indian residents, who pay slab rate)

Example – NRI Selling Inherited Property:

- Sale Price: ₹1 crore

- Capital Gain: ₹20 lakhs

- If LTCG: Tax = 20% = ₹4 lakhs

- If STCG: Tax = 40% = ₹8 lakhs (double the Indian rate!)

5. Reporting Requirements for NRIs:

- Must file Indian ITR if rental income > ₹5,000 (or any capital gain)

- Must report foreign bank accounts/assets under Schedule FA

- Need Indian Tax Return filing (even if income is zero in some cases)

Important: NRIs benefit from same inheritance rules as citizens but face higher capital gains tax for short-term gains. A tax consultant specializing in NRI taxation is critical.

How a Tax Consultant or Tax Planner Can Help You With Inherited Assets

A professional tax consultant or tax planner can significantly reduce your tax burden when dealing with inherited wealth. Here’s exactly how:

What a Tax Consultant Does:

1. Determines Fair Market Value (FMV) on Date of Death

- Tax consultants work with valuers to establish the exact FMV

- This becomes your “cost of acquisition” for capital gains purposes

- A higher FMV is better (results in lower capital gains when you sell)

- A lower FMV saves estate taxes (if applicable) but increases future capital gains

2. Plans Capital Gains Tax Timing

- Advises whether to sell immediately (when value hasn’t changed) or wait

- Calculates if Section 54 exemption applies

- Determines if holding period threshold affects LTCG vs. STCG

3. Structures Inherited Assets for Minimum Tax

- Suggests using Section 54 exemption (reinvest in residential property)

- Recommends Section 54EC bonds for capital gains deferral

- Advises on holding structure (individual vs. HUF vs. family trust)

4. Organizes Documentation

- Gathers will, death certificate, succession certificates

- Maintains records of cost basis adjustments

- Tracks CII (Cost Inflation Index) for indexation benefits

- Ensures all documents are ITR-compliant

5. Handles ITR Filing

- Files your income tax return accurately reflecting inherited income

- Reports rental income from inherited property

- Claims appropriate deductions and exemptions

- Avoids costly audit notices

6. Advises on Income Tax for Inherited Asset Income

- If inherited property generates rental income, tax consultant determines:

- What expenses are deductible (maintenance, property tax, insurance)

- Whether to claim depreciation (30% for residential, 40% for commercial)

- Best structure for claiming deductions

7. Manages NRI-Specific Rules (If Applicable)

- For NRIs inheriting Indian property, consultant handles:

- TDS compliance on rental income (30%)

- Higher capital gains tax for short-term gains (40% vs. 20% for Indians)

- Indian ITR filing requirements

- Foreign asset disclosure requirements

8. Prepares for Future Wealth Transfer

- Minimizing inheritance burden for your heirs

- Once you receive inherited assets, consultant advises on:

- How to structure them if you’ll pass to your children

- Whether to use trusts, gifts, or wills

Frequently Asked Questions About Inheritance Tax in India

Q1: Is there an inheritance tax in India?

A: No. India abolished inheritance tax (Estate Duty) in 1985. You do not pay any tax when you inherit property, money, or assets from a deceased family member. However, you will pay tax on income and gains generated from those assets.

Q2: Do I have to pay tax on inherited property?

A: Not on receiving it. But yes, on:

- Rental income (if the property generates rent)

- Capital gains (when you sell the property)

For example, if you inherit an apartment worth ₹1 crore and sell it for ₹1.2 crore, you pay 20% capital gains tax on the ₹20 lakh gain.

Q3: What is the difference between inheritance tax and capital gains tax?

A:

- Inheritance Tax: Tax on the transfer of assets at death (INDIA: 0%)

- Capital Gains Tax: Tax on the profit when you sell an asset (INDIA: 20% for LTCG, varies for STCG)

In India, there’s no inheritance tax, but capital gains tax applies when you sell inherited assets.

Q4: How is capital gains tax calculated on inherited property?

A:

- Cost of Acquisition = Fair Market Value on date of death

- Indexed COA = COA × (CII of sale year / CII of death year)

- Capital Gain = Sale Price – Indexed COA

- Tax = 20% of gain (if LTCG > 24 months holding) + cess + surcharge

We’ve provided a detailed worked example above.

Q5: What does “stepping up” cost basis mean?

A: It means the cost of acquisition is “stepped up” from the original purchase price to the Fair Market Value on the date of death.

Example:

- Father bought property for ₹10 lakhs in 2005

- Worth ₹1 crore when he dies in 2024

- Your cost basis = ₹1 crore (not ₹10 lakhs)

- If you sell immediately for ₹1 crore, gain = ₹0, tax = ₹0

This step-up is HUGE—it means you escape tax on all the appreciation during the original owner’s lifetime.

Q6: Can I use Section 54 exemption to avoid capital gains tax on inherited property?

A: Yes, if:

- The inherited property is residential

- You sell it and reinvest in another residential property

- The reinvestment happens within 2 years of sale

- You can claim 100% exemption on capital gains (up to the reinvestment amount)

Q7: What is Section 54EC, and how does it help?

A: Section 54EC allows you to invest up to ₹50 lakh per financial year in government securities to defer capital gains tax.

Benefit: 100% exemption on capital gains up to ₹50 lakh

Condition: You must invest within 6 months of selling the inherited asset, and hold for minimum 5 years.

Q8: Do I have to pay tax on inherited money in my bank account?

A: No, not on the principal amount. However:

- If the inherited bank account earns interest, that interest is YOUR taxable income

- Example: You inherit a ₹10 lakh FD earning 6%; the ₹60,000 annual interest is taxable to you

Q9: What about inherited life insurance?

A: Life insurance benefits are generally tax-free. The death benefit paid to you is not taxable income.

Exception: Some complex policies with loan components may have minor tax implications.

Q10: How does inheritance tax work for NRIs?

A:

- Inheritance itself: Tax-free (same as Indian citizens)

- Rental income: Taxable in India; 30% TDS is deducted

- Capital gains: LTCG = 20%, STCG = 40% (higher than Indians)

- NRI must file Indian ITR to report income/gains

Q11: Can the government reintroduce inheritance tax in India?

A: Technically yes, but unlikely in the near future:

- Economic arguments against it (evasion, capital flight)

- Political consensus against it (benefited middle class wealth transfer)

- Politicians periodically propose it but lack support

For current inheritance planning, assume inheritance tax remains at 0%.

Q12: What documents do I need to claim inherited assets and minimize taxes?

A:

- Will or succession certificate

- Death certificate of the deceased

- Valuation certificate from registered valuer (for property)

- Original purchase documents of the inherited asset

- Bank statements (if inheriting accounts)

- Insurance policy & claim forms (if inheriting insurance)

- Share certificates or mutual fund statements

Recommendation: Gather all documents and consult a tax consultant for ITR filing.

Q13: How long do I need to hold inherited property to qualify for long-term capital gains (LTCG) treatment?

A: The holding period includes BOTH:

- The time the original owner held it

- Your time as the heir

Total > 24 months = LTCG (20% tax with indexation benefit) Total ≤ 24 months = STCG (your income slab rate)

Example: If father held property 20 years before death, and you inherit it, ANY sale afterward qualifies for LTCG—you don’t need to hold it 24 more months.

Plan Your Inheritance Strategy With Fincart’s Wealth Management Experts

Inheritance is more than just receiving assets—it’s about strategically planning how to manage, optimize, and eventually pass on that wealth.

Fincart’s team of registered financial advisors and tax planners specialize in helping families navigate inherited wealth with minimal tax burden and maximum financial security.

What Fincart Can Help You With:

Inherited Asset Optimization

- Determine the optimal time to sell inherited property

- Structure reinvestment to minimize capital gains tax

- Plan use of Section 54 and Section 54EC exemptions

- Document FMV properly to maximize indexation benefits

Multi-Generational Wealth Planning

- Create tax-efficient structures for passing inherited wealth to your children

- Explore family trusts, HUFs, and other legal structures

- Plan for long-term family wealth accumulation

Family Business Succession

- Structure business succession if you inherited a family business

- Plan entity restructuring to minimize tax on future transfers

- Advise on business valuations and succession documentation

Legacy & Estate Planning

- Create a comprehensive estate plan for your own wealth

- Ensure smooth wealth transfer to your heirs (minimizing what THEY’ll pay in capital gains tax)

- Structure your will, trusts, and succession certificates

Personalized Tax Optimization

- Custom strategies based on your specific inheritance scenario

- NRI-specific planning if you’re an NRI inheriting in India

- Cross-border wealth management for international assets

Documentation & Compliance

- Organize all inheritance documentation for tax purposes

- Ensure ITR filing is accurate and audit-proof

- Maintain proper cost basis records for future sales

Why Choose Fincart?

✓ AMFI-Registered Advisors: All our financial advisors are certified and regulated

✓ Tax Expertise: Our team includes chartered accountants and tax specialists

✓ Holistic Approach: We don’t just handle inheritance; we plan your entire financial future

✓ India-Focused: Deep expertise in Indian personal finance, tax law, and wealth management

✓ Transparent Fees: Clear, upfront pricing with no hidden charges

Next Step: Schedule Your Inheritance Planning Consultation

Every inheritance scenario is unique. Your needs depend on:

- How much you inherited

- What type of assets (property, business, investments)

- Your future plans (keep, sell, expand)

- Your tax bracket and family structure

- Whether you’re an NRI or resident Indian

[Schedule a Free Consultation with a Fincart Wealth Advisor]

During a 30-minute consultation, we’ll:

- Understand your specific inheritance situation

- Identify tax optimization opportunities

- Recommend strategies customized to your goals

- Explain next steps for implementation

Quick Answer: Inheritance Tax in India at a Glance

The most important thing to know about inheritance tax in India:

✓ No Inheritance Tax: India abolished Estate Duty (inheritance tax) in 1985. You do NOT pay any tax when you inherit property, money, or assets from a deceased family member.

✓ But Income IS Taxable: Rental income, dividend income, and interest earned from inherited assets become YOUR taxable income and must be reported to the tax authorities.

✓ Selling Property = Capital Gains Tax: When you sell inherited property, you pay capital gains tax—typically 20% for long-term gains (with inflation indexation benefit) or according to your income slab for short-term gains.

✓ Gift Tax Still Exists: If you inherit through a will or succession, it’s NOT treated as a gift. However, if someone gives you money/assets as a gift (outside of inheritance), different rules may apply.

✓ Documentation Matters: Keep all inheritance documents, original valuations, and cost basis records. These are critical for claiming indexation benefits and minimizing capital gains tax.

Bottom Line: You save on inheritance tax, but you’ll pay tax on the income and gains generated from those inherited assets.