Planning for retirement is no longer optional—it is one of the most important financial goals for every Indian. Rising inflation, increasing healthcare costs, and longer life expectancy mean you need a retirement corpus that can support your lifestyle for decades after you stop working. Among the most popular retirement savings options in India are the Employees’ Provident Fund (EPF), Public Provident Fund (PPF), and the National Pension System (NPS). Each scheme offers unique benefits in terms of returns, taxation, liquidity, and risk. If you’re searching for EPF vs. PPF vs. NPS, you’re likely trying to answer one key question:

Which retirement investment option is best for your financial goals?

The answer depends on factors such as your employment status, income level, retirement timeline, tax bracket, and risk appetite.

In this comprehensive guide, you’ll learn:

- How each scheme works

- Latest interest rates and tax benefits

- Expected returns

- Withdrawal rules

- Ideal investors for each option

- When to combine multiple retirement products

- How a financial consultant or retirement plan services provider can help optimize your retirement strategy

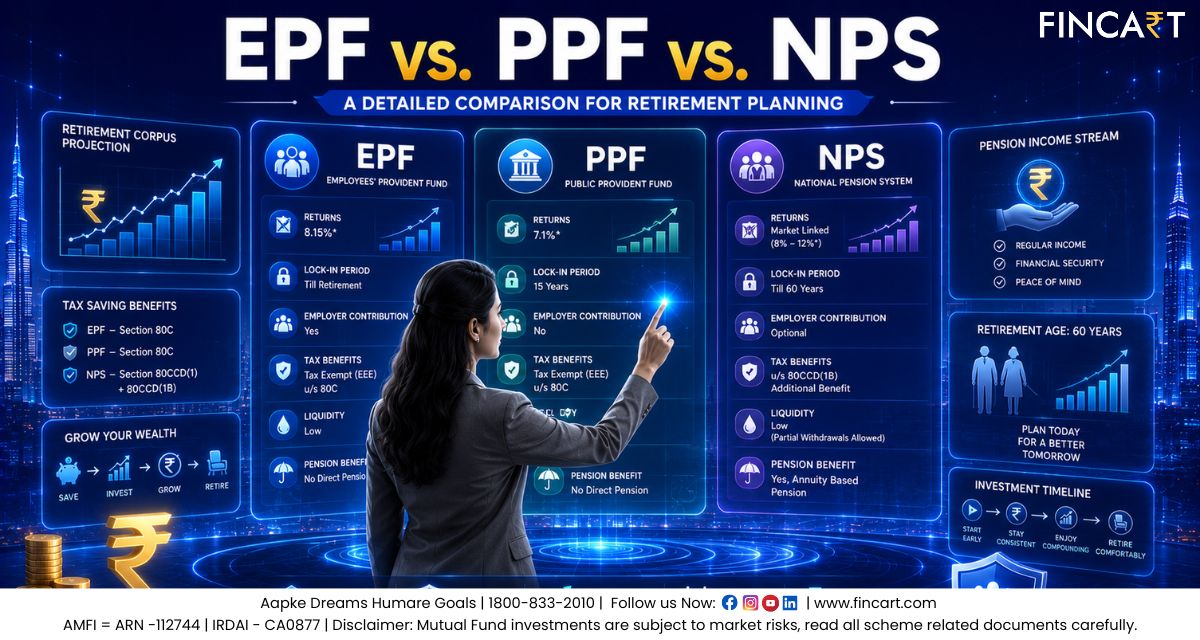

Recent updates show that the EPF interest rate remains at 8.25% for FY 2025–26, while the PPF interest rate continues at 7.1%, and NPS remains a market-linked retirement product with the potential to generate higher long-term returns, albeit with market risk.

Why Retirement Planning Matters More Than Ever

Retirement planning is about replacing your salary with sustainable income.

Consider this example:

Suppose you’re 30 years old and spend ₹60,000 every month.

Assuming 5% annual inflation, your monthly expenses could exceed ₹2.5 lakh by the time you retire at age 60. Without disciplined investing, maintaining the same lifestyle can become challenging.

A sound retirement strategy should aim to:

- Beat inflation

- Generate long-term wealth

- Provide tax efficiency

- Offer adequate liquidity for emergencies

- Create a predictable income stream after retirement

This is why understanding the differences between EPF, PPF, and NPS is essential.

What is EPF (Employees’ Provident Fund)?

The Employees’ Provident Fund (EPF) is a government-backed retirement savings scheme managed by the Employees’ Provident Fund Organisation (EPFO) under the Ministry of Labour and Employment.

It is primarily designed for salaried employees working in eligible establishments.

How EPF Works

Both the employee and employer contribute a portion of the employee’s Basic Salary plus Dearness Allowance every month.

Typically:

- Employee Contribution: 12%

- Employer Contribution: 12% (split between EPF and EPS)

These regular contributions accumulate over your working years and earn annual interest declared by the EPFO.

For FY 2025–26, the EPF interest rate has been retained at 8.25%, continuing one of the highest government-backed fixed-income returns in India.

Key Features of EPF

| Feature | Details |

|---|---|

| Scheme Type | Government-backed |

| Eligibility | Salaried employees |

| Interest Rate | 8.25% (FY 2025–26) |

| Risk | Very Low |

| Employer Contribution | Yes |

| Tax Benefit | Eligible under Section 80C |

| Maturity | Retirement |

Advantages of EPF

1. Employer Contribution

Unlike other retirement products, your employer also contributes to your retirement savings, helping your corpus grow faster.

2. Attractive Returns

Historically, EPF has delivered higher fixed returns than many traditional debt products.

3. Triple Tax Benefit

Subject to applicable conditions:

- Contributions qualify for deductions under Section 80C.

- Interest earned is generally tax-free.

- Eligible withdrawals are tax-free.

4. Automatic Savings

Monthly payroll deductions encourage disciplined investing.

Limitations of EPF

- Available mainly to salaried employees.

- Limited investment flexibility.

- Premature withdrawals are restricted.

- Excess contributions beyond prescribed limits may attract tax implications.

Who Should Invest in EPF?

EPF is ideal for:

- Salaried professionals

- Employees seeking stable returns

- Individuals preferring low-risk retirement savings

- Investors looking for tax-efficient long-term wealth creation

What is PPF (Public Provident Fund)?

The Public Provident Fund (PPF) is one of India’s most trusted long-term savings schemes, backed by the Government of India.

Unlike EPF, PPF is open to almost every resident Indian, including self-employed individuals, professionals, and those without employer-sponsored retirement benefits.

How PPF Works

You can invest between ₹500 and ₹1.5 lakh per financial year in a PPF account.

The account has a 15-year maturity, with the option to extend it in blocks of five years.

The current PPF interest rate is 7.1% per annum, compounded annually. The government reviews this rate every quarter.

Key Features of PPF

| Feature | Details |

|---|---|

| Scheme Type | Government-backed |

| Eligibility | Resident Individuals |

| Interest Rate | 7.1% |

| Risk | Virtually Risk-Free |

| Lock-in | 15 Years |

| Tax Benefit | EEE (Exempt-Exempt-Exempt) |

Advantages of PPF

Guaranteed Returns

Since the Government backs PPF, there is virtually no default risk.

Complete Tax Exemption

PPF enjoys EEE status:

- Investment qualifies for Section 80C deduction.

- Interest earned is tax-free.

- Maturity proceeds are tax-free.

Excellent for Conservative Investors

PPF suits individuals who prioritize capital protection over aggressive growth.

Flexible Contributions

You can contribute according to your financial capacity, making it suitable for freelancers and self-employed professionals.

Limitations of PPF

- Annual investment capped at ₹1.5 lakh.

- Long 15-year lock-in period.

- Returns may not always outpace inflation significantly over extended periods.

Who Should Invest in PPF?

PPF is best suited for:

- Self-employed individuals

- Freelancers

- Small business owners

- Conservative investors

- Parents saving for long-term family goals

What is NPS (National Pension System)?

The National Pension System (NPS) is a market-linked retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

Unlike EPF and PPF, NPS invests in a diversified portfolio that may include:

- Equity

- Corporate Bonds

- Government Securities

- Alternative Investments

Because of this diversified allocation, NPS offers higher long-term wealth creation potential but also involves market risk.

How NPS Works

You contribute regularly during your working years.

Professional pension fund managers invest your money according to your chosen asset allocation.

At retirement:

- Up to 60% of the corpus can generally be withdrawn as a lump sum (subject to prevailing regulations and tax provisions).

- At least 40% is typically used to purchase an annuity, providing a regular pension income.

Key Features of NPS

| Feature | Details |

|---|---|

| Scheme Type | Market-linked |

| Regulator | PFRDA |

| Risk | Moderate to High |

| Lock-in | Until retirement (with permitted exit rules) |

| Tax Benefits | Sections 80CCD(1), 80CCD(1B), and employer contribution under 80CCD(2) |

| Returns | Market-linked |

Advantages of NPS

- Higher Wealth Creation Potential– Exposure to equities can generate better inflation-adjusted returns over the long term.

- Additional Tax Benefit – NPS offers an additional deduction of up to ₹50,000 under Section 80CCD(1B), over and above the ₹1.5 lakh limit under Section 80C.

- Professional Fund Management – Your investments are managed by regulated pension fund managers.

- Flexible Asset Allocation – Investors can choose between active and auto-choice investment options.

Limitations of NPS

- Returns are not guaranteed.

- Mandatory annuity purchase reduces liquidity at retirement.

- Pension income from annuity is taxable as per applicable laws.

- Market volatility can impact returns.

Who Should Invest in NPS?

NPS is suitable for:

- Young professionals

- Investors with a long investment horizon

- Individuals comfortable with moderate market risk

- Taxpayers seeking additional tax deductions

- Those aiming to build a larger retirement corpus through market participation

EPF vs. PPF vs. NPS: Key Comparison

| Feature | EPF (Employees’ Provident Fund) | PPF (Public Provident Fund) | NPS (National Pension System) |

|---|---|---|---|

| Scheme Type | Govt. pension fund (EPFO, labour ministry) | Govt. small savings scheme (Ministry of Finance) | Market-linked pension (PFRDA-regulated) |

| Eligibility | Salaried employees in EPF-registered establishments | Any resident Indian (individual) | All Indians (18–65), NRI eligible (Tier I) |

| Contribution | Employee 12% of basic+DA + Employer (12%, of which 8.33% to EPS) | Voluntary (₹500 – ₹1.5 lakh/yr) | Voluntary (Tier I: ₹1,000/yr min; Tier II: ₹250) |

| Employer Contribution | Yes (12% of basic, partly to EPF & EPS) | No | Yes (up to 10% basic+DA) – eligible under 80CCD(2) |

| Returns | Fixed 8.25% p.a. for FY 2025–26 | Fixed 7.10% p.a. (compounded annually) | Market-linked; equity 9–12% (past decade), debt ~7–9%; no guarantee |

| Risk Level | Very Low (government-guaranteed) | Very Low (government-guaranteed) | Moderate/High (subject to market volatility) |

| Lock-in / Tenure | Until retirement or 5 continuous yrs (whichever later) | 15 years (with 5-year lock-in) | Tier I: Until age 60 (partial allowed); Tier II: No lock-in |

| Liquidity | Partial withdrawal/loans allowed (housing, edu., etc.) | Partial withdrawal allowed from 5th year (max 50% of balance) | Partial withdrawal 25% after 3 yrs for specific reasons |

| Tax Benefits | Exempt-Exempt-Exempt (E-E-E): ₹1.5L deduction (80C); interest & maturity tax-free (if 5+ yrs) | E-E-E: ₹1.5L deduction (80C); tax-free interest and maturity | Exempt-Exempt-Tax (E-E-T): Deduction up to ₹2L (80C+80CCD); 60% lump sum tax-free; annuity taxed |

| Withdrawal Taxation | Tax-free if withdrawn after 5 yrs service; else partially taxable | Entire corpus tax-free at maturity | 60% of corpus tax-free; rest used to buy annuity (annuity payouts taxed) |

| Fees/Charges | Nil (no fund management fees) | Nil | Low: fund management |

| Ideal for | Salaried workers seeking safe, automatic savings | Self-employed or conservative investors wanting assured returns | Long-term investors seeking higher retirement corpus; high-income/taxpayers seeking extra deduction |

Returns Comparison

- EPF (8.25% fixed) – The EPF yield is stable and guaranteed by the government. The 8.25% rate for FY 2025–26, compounded annually, means a steady real return (above inflation most years) with very low risk. For example, ₹1 lakh invested each year at 8.25% would grow to about ₹1.28 crore in 30 years (inflation aside). The EPF’s partial allocation to government and corporate bonds (and some equity ETF investments) has enabled it to maintain 8%+ returns consistently.

- PPF (7.1% fixed) – PPF offers a guaranteed 7.1% per annum (compounded yearly). This is fully tax-free and risk-free, making PPF slightly safer but with lower returns than EPF. In long-term scenarios, EPF outpaces PPF by ~1.1% annually (8.25 vs 7.1%). Over 25 years of investing ₹1 lakh/year, for example, EPF could yield ~₹82.1 Lakh vs PPF’s ~₹68.7 Lakh (nominal).

- NPS (market-linked) – NPS returns depend on asset allocation. Tier I scheme offers options from 100% equities to conservative debt mixes. Historically, equity-oriented NPS funds have delivered ~12–16% annualized over 5–10 years, whereas government bond funds yield ~7–9%. For instance, one leading NPS equity fund averaged ~16.3% over 5 years.

- If a young investor invests ₹1 lakh/year in an aggressive NPS (≈10% average return), they might accumulate ~₹1.81 Crore in 30 years (taxes aside), significantly more than EPF/PPF. However, market volatility means annual returns can swing. NPS explicitly has no guaranteed returns, but offers higher growth potential for long-term goals.

In summary, EPF/PPF give certainty and beat many FDs/POs, but NPS can potentially build a much larger corpus (at higher risk and effort managing allocation). Many experts suggest combining them: e.g., safe base of EPF+PPF plus a dedicated NPS allocation for growth.

Tax Benefits Comparison

- EPF: Employee contributions (and voluntary contributions to EPF/Voluntary PF) are deductible under Section 80C (up to ₹1.5 lakh). The interest earned and withdrawal amount (at retirement) are generally tax-free, provided you have been in service for the requisite period (5 years of service) and conditions are met (making EPF effectively an EEE instrument).

- PPF: Contributions qualify for Section 80C deduction (up to ₹1.5 lakh). Both the interest and the final maturity corpus are completely tax-free. PPF is a classic EEE (Exempt-Exempt-Exempt) scheme: you save tax on investment, earn tax-free interest, and withdraw tax-free.

- NPS (Tier I):

- Section 80CCD(1): Employee contributions deductible up to 10% of salary (basic+DA) within the ₹1.5 lakh 80C limit.

- Section 80CCD(1B): Extra deduction of ₹50,000 (over and above 80C limit) for self-contribution to NPS. This is a key advantage – effectively allowing up to ₹2 lakh in deductions (1.5L+50k).

- Section 80CCD(2): Employer contributions (for salaried) deductible up to 10% of salary (14% under new regime). These are exempt from tax but capped by employer’s policy.

- Withdrawals: Up to 60% of the pension corpus withdrawn at retirement is tax-exempt. However, the remaining ~40% must be used to buy an annuity; future annuity payments are taxable. Also, partial withdrawals (25% of contributions after 3 years) are tax-free. Thus NPS offers 3 layers of benefit: 80C+80CCD(1B), plus 60% lump sum tax-free.

Key takeaway: For tax-saving, EPF/PPF each give ₹1.5 lakh under 80C. NPS extends that by ₹50k extra for high-income earners. In practice, one can invest ₹1.5L in PPF/EPF and also ₹50k in NPS for full benefits.

Liquidity & Withdrawal Rules

- EPF: Very liquid in emergencies for salaried employees. While the full EPF balance is ideally withdrawn at retirement, members can take partial advances or withdrawals for prescribed reasons (housing loan down-payment, medical treatment, marriage, education, etc.) after 5 years of service. These partial withdrawals are usually not taxable. If you switch jobs or retire early, you can also withdraw the full balance (with employer’s consent and applicable taxes).

- PPF: Locked for 15 years, but not entirely illiquid. After 6 financial years from account opening, you can make partial withdrawals (up to 50% of balance from 4 years ago). Also, loans (up to 25% of balance) are available between years 3–6. Premature closure (before 15 years) is only allowed for specific reasons (higher education, medical). Unlike EPF, there’s no employer role – just your deposits. After 15 years (and any extensions), you can withdraw the entire tax-free corpus.

- NPS (Tier I):Lock-in until retirement (60 years) is the norm. Partial withdrawals (25% of your own contributions) are allowed after 3 years, but only for limited purposes (medical treatment, children’s education/marriage, or unemployment) and capped at 3 withdrawals in a lifetime.

- At retirement (60+): You may take up to 60% of your accumulated corpus in a lump sum (completely tax-free), and must purchase an annuity with the remaining ~40% (getting a regular pension). The annuity payments are taxable as income.

- Exit before 60: Allowed after 10/15 years with strict conditions – typically Government subscribers must exit only at 60, while others can exit after 10 years by buying annuity on exit and taking 20–60% lump sum (depending on total corpus).

In short, EPF is fairly liquid with loans/advances, PPF has long lock-in with limited withdrawals, and NPS is locked (with retirement exit rules). EPF/PPF provide easier access to funds (especially EPF), whereas NPS primarily builds long-term retirement corpus.

Who Is It Best For?

- EPF: Ideal for salaried professionals who want a low-risk retirement corpus plus tax benefits. If you have a regular job that contributes to EPF, it’s smart to maximize your employee and even voluntary contributions, since your employer matches 12% and the returns (~8.25%) beat most fixed-income products. EPF is great “automated savings” — you rarely have to think about it once payroll deductions start.

- PPF: Best suited to self-employed, freelancers, small business owners, or anyone who lacks employer retirement benefits. PPF’s guaranteed returns and triple tax shield (80C deduction + tax-free interest/maturity) make it a perfect conservative building block. It’s also good as an overflow fund – after hitting the ₹1.5L 80C limit, extra investments can still go into PPF for safety. Parents or joint account holders can use PPF to save for children’s long-term goals.

- NPS: Suited for young investors with long time horizons, higher risk tolerance, and those in higher tax brackets looking for extra deductions. If you’re comfortable with equity investing, NPS lets you choose lifecycle funds with up to 75% equity, boosting growth potential (and beats inflation). High-income earners benefit from the extra ₹50k deduction (80CCD(1B)). For example, a 30-year-old wanting a big retirement corpus might allocate 70% to NPS equity (E) and 30% to debt (C/G), enjoying both tax breaks and market returns.

- Combination: Many financial planners recommend using all three: Keep your EPF active via your job, use PPF for additional safe savings, and start an NPS account for extra tax savings and equity exposure. For instance, one could invest ₹1.5 lakh in PPF/EPF and an additional ₹50k in NPS Tier I to fully leverage tax incentives.

- Example Use-Case: Rahul (35, software engineer) has no EPF (private employer), invests ₹18,000 monthly (₹2.16L/year). A mix could be: ₹1.5 lakh into PPF for guaranteed growth, and ₹66k in NPS with 75% equity (securing ₹50k tax break). Over 25 years, this balance of safety and growth could yield a corpus supporting a comfortable retirement.

In summary: Use EPF if you have a regular salary; PPF for absolute safety and tax-free returns; NPS if you want a higher growth engine plus extra tax perks. Choose based on your risk profile and retirement goals, and consult a financial consultant to allocate among them optimally.

Pros & Cons

Employees’ Provident Fund (EPF)

- Pros: Guaranteed returns higher than FDs (8.25% in FY26). Employer matching doubles savings rate. Full tax benefits (80C + tax-free withdrawals). No equity risk – government guarantee. Auto payroll deduction builds discipline.

- Cons: Only available to salaried employees. Very limited investment choice (all pooled in EPFO funds). Withdrawals and transfers can be bureaucratic. Corpus locked until retirement (though advances allowed after 5 years).

Public Provident Fund (PPF)

- Pros: 100% sovereign guarantee; principal and returns are fully secure. Tax-free at all stages (EEE status). Flexible deposit (even ₹500 min) suits any saver. Partial withdrawals and loans available after minimum period. Long track record of stable 7–8% returns.

- Cons: Annual deposit cap of ₹1.5 lakh. Long lock-in (15 years) deters liquidity. Returns (7.1%) might barely beat inflation over decades. No pension – only lump-sum payoff.

National Pension System (NPS)

- Pros: Market-linked growth with equity upside (can outperform EPF/PPF long-term). Extremely low costs (TER ~0.01% for Tier I). Additional ₹50,000 tax deduction (80CCD(1B)). Flexible asset allocation (active or auto), portability across jobs. Tier II option for post-tax investments (no lock-in).

- Cons: No guaranteed returns; susceptible to market downturns (e.g., 2020 losses then recovery). Mandatory annuity purchase reduces liquidity at retirement. Annuity payments are taxable (only 60% corpus is tax-free). More complex product – requires active decisions or advice. Premature exit rules are restrictive.

Each scheme has strengths: EPF is almost like a forced savings (best for employees), PPF is ultra-safe, and NPS is a growth engine with more complexity. Your choice (or combination) should match your priorities: security vs. growth, short-term access vs. long-term accumulation.

Frequently Asked Questions (FAQ)

- What is the difference between EPF, PPF, and NPS?

EPF and PPF are fixed-return government schemes (8.25% and 7.1%, respectively) primarily for retirement savings, whereas NPS is a market-linked pension scheme offering equity and debt exposure. EPF involves employer contribution; PPF is voluntary; NPS provides extra tax deductions (80CCD). - Which is safer: EPF or PPF?

Both are very safe (sovereign-backed). EPF’s stability is proven by consistent 8%+ rates. PPF is equally secure with slightly lower yield. Choose EPF if you have employer coverage; choose PPF if you need flexibility (self-employed, or when EPF contributions max out tax benefits). - Is NPS better than PPF? When should I use NPS?

NPS has the potential for higher returns (due to equity investment) but also higher risk. Use NPS if you have a long horizon (20+ years) and can endure market swings, and if you want an extra ₹50k tax break. For purely risk-averse savers, PPF may be preferable. - Can I invest in EPF and PPF both?

Yes. In fact, doing so is a common strategy: EPF (via your job) plus PPF on the side. You can claim up to ₹1.5L in combined 80C deductions (covering both EPF & PPF). Some people max out EPF and put any extra tax-saving money into PPF. - Are EPF withdrawals taxable?

EPF withdrawals at retirement (or after 5 years of service) are tax-free. Partial EPF withdrawals for approved reasons are also tax-exempt. Voluntary contributions and interest within EPF are also tax-free. (This contrasts with NPS, where only 60% of the retirement corpus is tax-free.) - Can I transfer my EPF and PPF when I change jobs?

EPF: Yes – your EPF account (Universal Account Number, UAN) stays with you across jobs; you just update your employment details. You can also claim PF advances between jobs if needed.

PPF: You cannot “transfer” a PPF between banks, but you can open a new account and manually move funds (usually not needed if using the same nationalized bank or post office). PPF follows you anyway – it’s under your name, not your employer. - What happens to my NPS when I retire?

At retirement (60 years), you can withdraw up to 60% of your NPS corpus as a lump sum (tax-free). The remaining 40% is mandatorily used to purchase an annuity (providing a pension). You can choose from different annuity providers. The annuity income you receive will be taxed as per your slab. - Can I take a loan against PPF or EPF?

- PPF: Yes, you can take a loan up to 25% of your balance between the 3rd and 6th year of account opening. After that, PPF only allows withdrawals, not loans.

- EPF: EPF allows advances (not technically loans) for specific purposes like housing, education, medical after 6 months to 5 years of service. The limit depends on your salary and contributions.