What Is Zero-Based Budgeting?

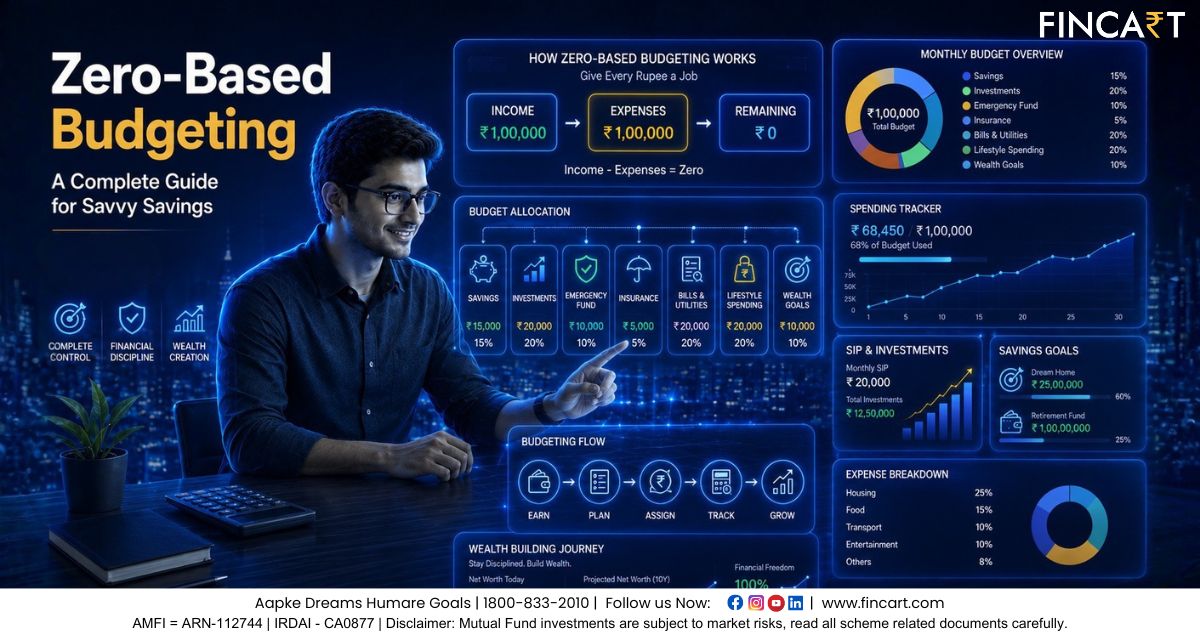

Zero-based budgeting (ZBB) is a budgeting method where every rupee of income is assigned a purpose from a “zero base” each period. Unlike traditional incremental budgeting (which adjusts last year’s numbers), ZBB requires justifying all expenses from scratch for each new month or year. In practice, you list your total income and then allocate every unit (dollar, rupee, etc.) to expenses, savings, or debt until the balance is zero. This means at the end of planning, income minus allocations equals zero – hence “zero-based” budgeting. For example, if your monthly income is ₹60,000, you might allocate ₹10,000 to rent, ₹6,000 to groceries, etc., until no unassigned income remains.

Pete Pyhrr, a manager at Texas Instruments, popularized zero-based budgeting in the 1970s, and both individuals and companies have since used it to improve cost discipline. As one corporate finance resource explains, ZBB treats every expense as discretionary and requires a strategic justification for each line item. In short, ZBB forces you to “give every rupee a job” and decide ahead of time where it will go.

Why Use Zero-Based Budgeting? (Benefits)

Zero-based budgeting offers unparalleled control and clarity over your finances. Its benefits include:

- Full Spending Visibility: By planning every expense, you get a clearer view of your financial picture. ZBB forces you to examine each cost, so you might discover you’re paying for unused subscriptions or duplicate services. This can help eliminate wasted spending (e.g. multiple streaming services).

- Intentional Savings: With ZBB, you “pay yourself first” by allocating savings and investments at the start of budgeting. Instead of saving whatever is left, you decide upfront to put aside, say, 10–20% of income. This proactive approach can boost savings rates and ensure long-term goals (like emergency funds or retirement) are funded.

- Customized Flexibility: Unlike rigid percentage rules (e.g. 50-30-20), ZBB is highly adaptable. You set rules each month based on your current needs. For example, if income or priorities change, you can reallocate funds without fixed split rules constraining you. This flexibility can benefit irregular-income earners (freelancers, gig workers) who need to adjust budgets frequently.

- Better Decision-Making: By scrutinizing every category, ZBB promotes active financial decision-making and discipline. You intentionally plan indulgences (like dining out) rather than letting them happen by chance. This can curb impulse spending and help stick to financial goals.

- Adaptable to Goals: Since each rupee is purposeful, ZBB can accelerate debt repayment or savings when needed. For instance, if aiming to pay off an EMI faster, you can allocate extra rupees there first. This makes it a powerful tool for turning specific goals (debt freedom, down payment, etc.) into action plans.

In summary, ZBB gives you total control over your money and ensures every expense aligns with your priorities. It promotes financial discipline and helps uncover unnecessary spending. Many financial planners and consultants in India recommend this method for people who want the maximum clarity and efficiency in budgeting.

Drawbacks of Zero-Based Budgeting

While powerful, ZBB has some downsides to consider:

- Time-Consuming: Zero-based budgeting requires detailed planning and tracking. You must list every income source and expense category and adjust allocations precisely. Especially at first, this can feel labor-intensive.

- Can Be Rigid: Because every rupee is pre-planned, ZBB can be less flexible on a day-to-day basis. If an unexpected expense occurs, you must shuffle allocations or dip into an emergency fund (which should already be planned for, ideally).

- Stressful if Not Followed: If you skip tracking or overspend, ZBB can become complex and unsustainable. Mint Money warns that if not followed, ZBB “becomes complex” and loses its effectiveness.

- Not Always Fun: Some people may find ZBB too strict. It requires you to say no to unplanned desires once you set the budget. This level of discipline may not suit everyone’s personality or lifestyle.

- Possible Overhead: For businesses, ZBB can be bureaucratic (building many “decision packages” for each cost). For individuals, using multiple apps or spreadsheets can feel like overhead.

Overall, the cons boil down to effort and discipline. ZBB works best for those committed to thorough budgeting. If you prefer more free-wheeling methods or don’t want to plan every detail, simpler systems (like the 50-30-20 rule) might suit you better.

How to Create a Zero-Based Budget: Step by Step

Implementing a zero-based budget is methodical. Here’s a step-by-step process you can follow:

- List All Income Sources. Calculate your total monthly income from every source: salary, business, interest, side gigs, etc. Example: Mr. P’s total income is ₹60,000 (₹50,000 salary + ₹5,000 interest from FD + ₹5,000 tutoring). (See example breakdown below.)

Figure: Example breakdown of monthly income for a zero-based budget (source: Gripinvest) - List All Expenses, Savings, and Debts. Write down every expense category you have. Include fixed costs (rent, EMIs, utilities) and variable costs (groceries, dining, entertainment). Also list savings goals (emergency fund, mutual funds, etc.) and debt payments. Don’t forget occasional categories (insurance premiums, gifts). Be comprehensive.

- Fixed Expenses: Rent/mortgage, loan EMIs, insurance, subscriptions (Netflix, etc.), school fees, utilities.

- Variable Expenses: Food, transport, shopping, entertainment, travel.

- Goals/Savings: Emergency fund, investments, vacation fund, charity.

- Debt Repayment: Credit card bills, personal loans, etc.

- Allocate Every Rupee Until the Balance is Zero. Start assigning your income to each item on the list. Typically:

- Cover essentials first: Allocate fixed expenses (rent, EMIs) fully. Allocate savings/debt next: Decide how much to save or invest and pay toward debt. It requires you to say no to unplanned desires once you set the budget. Assign remaining to variable or discretionary expenses. Adjust amounts so that sum of all allocations equals your total income. If you reach the end and have leftover income, allocate more to savings or pay down debt further. If allocations exceed income, you must trim discretionary spending.

- Monitor and Adjust Monthly. Every month, review actual spending against the plan. If you under- or overspend in a category, adjust the next month’s budget. ZBB encourages regular reviews so your budget stays realistic. Use bank statements or apps to track expenses.

By following these steps each budgeting cycle (monthly or yearly), you ensure every source of money is purposefully used. This process may require effort initially, but it becomes quicker as you get used to it.

Zero-Based Budgeting vs Other Methods

| Method | Core Principle | Best For | Pros | Cons |

|---|---|---|---|---|

| Zero-Based Budgeting (ZBB) | Assign every rupee to an expense or goal; start each period from zero | Aggressive savers, debt paydown, seasoned planners | Maximum spending control; uncovers waste; adapts to changing needs | Time-consuming; requires strict tracking and discipline |

| 50-30-20 Rule | 50% needs, 30% wants, 20% savings | Beginners, stable incomes | Simple, easy split; minimal tracking | May not fit all lifestyles; less precise |

| Envelope Budgeting | Fixed cash limits for each spending category | Impulse spenders; visual learners | Strong curb on overspending in each category | Inconvenient without cash (or app); inflexible once envelope is empty |

| Incremental Budgeting | Build on last period’s budget with small changes | Traditional approach; businesses/governments | Easy to maintain if few changes; familiar | Can perpetuate inefficiencies; little accountability |

Adapted features from Mint Money and GripInvest. For example, Mint’s analysis shows ZBB offers “total control of every rupee,” but requires “dedicated tracking”. In contrast, the 50-30-20 rule is easier but less tailored. Envelope budgeting caps spending effectively, but is often done with cash or apps for each category. Each method has trade-offs, so choose based on your goals and lifestyle.

Tools, Apps, and Financial Planners

You can do zero-based budgeting with paper, spreadsheets, or apps. Many digital tools can simplify the process:

- Spreadsheets: Google Sheets or Excel templates allow full customization. You can build your own ZBB template easily.

- Budgeting Apps: Apps like Goodbudget (envelope-style), Wallet, or Mint (US-based) can be adapted for ZBB by setting category budgets. In India, apps like Walnut or MoneyView help track expenses by linking bank accounts.

- Expense Trackers: Use apps or bank SMS alerts to monitor spending in real-time.

- Calculators: Online ZBB calculators (e.g. MintByte’s Zero-Based Budget Calculator) can guide the first budget setup.

Regardless of tools, consistency is key. Financial planning services often include budgeting as part of their offerings. A certified financial planner or financial consultant in India can help set up a zero-based budget aligned with your goals. They can account for taxes, investments, insurance, etc., ensuring you allocate each rupee effectively. If you feel overwhelmed, consider seeking advice from a CFP or a reputable financial advisor who offers budgeting guidance.

ZBB in Business and Government

Zero-based budgeting extends beyond personal finance. Many companies use ZBB for cost management. For example, Bain & Company notes that firms adopting ZBB can cut their cost base by ~25% and enjoy 150% higher returns over time. This shows how disciplined budgeting drives significant savings and growth. However, corporate case studies also warn: Kraft Heinz’s strict ZBB led to cutting innovation and brand value, whereas Unilever’s balanced “Save to Grow” approach ring-fenced key projects and reinvested savings.

In India’s public sector, ZBB has been applied too. In 2017, the government’s NITI Aayog implemented zero-based budgeting for national schemes. This reform meant “every scheme must justify every rupee,” pruning outdated programs and reallocating funds to priority projects like Digital India, GST rollout, and rural electrification. In other words, India shifted from incremental to zero-based budgeting to focus spending on outcomes and efficiency.

These examples highlight that ZBB works for anyone – from households to large organizations – who want a rigorous framework for financial decision-making.

Summary of Key Points

- Business use: Companies and governments also apply ZBB to optimize costs (e.g. India’s 2017 budget reform).

- Zero-based budgeting (ZBB) means assigning every rupee of income a specific purpose, so income minus expenses equals zero.

- Benefits: full control and clarity of spending, intentional saving first, and tailored budgeting (no unallocated cash).

- Drawbacks: requires more time and discipline; can be rigid and complex if not maintained.

- Implementation: 1) List all income sources, 2) List expenses (fixed/variable), savings and debts, 3) Allocate funds to each item until total equals income.

- Comparison: Unlike the 50-30-20 rule or incremental budgeting, ZBB gives maximal control but demands detailed tracking. It’s ideal for debt reduction or goal-focused savers, while simpler methods may suit casual budgets.

- Professional advice: Financial planners and financial planning services in India often use ZBB principles. A certified financial consultant can assist in customizing your budget.

FAQs About Zero-Based Budgeting

Q: What is zero-based budgeting?

A: Zero-based budgeting (ZBB) is a method where you budget from scratch each period, assigning every rupee of income to specific expenses, savings, or debts so that income minus allocations equals zero.

Q: How do I start a zero-based budget?

A: First, calculate your total monthly income. Then list all expenses (rent, bills, groceries, etc.), plus savings and debt payments. Allocate your income to each item until no money is left unassigned. Use a spreadsheet or app to help track categories.

Q: What are the benefits of zero-based budgeting?

A: ZBB provides maximum control over spending. It helps identify waste, ensures you save first, and aligns spending with goals. It also adapts easily to changing income or priorities.

Q: What are the disadvantages of zero-based budgeting?

A: It can be time-consuming and requires discipline. You must plan in detail and track expenses closely. If you lose focus, the method can become cumbersome or fall apart.

Q: When should I use zero-based budgeting?

A: ZBB is best when you need strict control—such as when paying off debt, saving aggressively, or managing irregular income. It’s especially useful if you find money slipping away and want to understand exactly where every rupee goes.

Q: How does zero-based budgeting differ from the 50-30-20 rule?

A: The 50-30-20 rule sets fixed percentages for needs (50%), wants (30%), and savings (20%). ZBB, by contrast, involves zero-based allocation without preset ratios. ZBB can accommodate different percentages each month, giving more flexibility but requiring more effort.

Q: Can I do zero-based budgeting on my own?

A: Yes, anyone can implement ZBB. However, consulting a financial planner or financial consultant can be helpful for personalized guidance, especially to address tax, investment, and long-term financial planning aspects.

Q: What if my income changes month to month?

A: With variable income, you can still use ZBB by first setting a baseline budget based on expected income, then adjusting allocations each month. Always cover fixed needs first, and adjust wants/savings if income is lower.

Q: Is there software for zero-based budgeting?

A: Many budgeting apps (Goodbudget, YNAB, etc.) and spreadsheets can be used for ZBB. Some online calculators (e.g. MintByte) also exist. The key is tracking every expense category until the budget balances to zero.