Why Gen Z in India Is Rewriting the Investment Playbook

India’s Gen Z — those born between 1997 and 2012 — is the most financially aware young cohort the country has ever produced. Gen Z investing in India has been on a rise

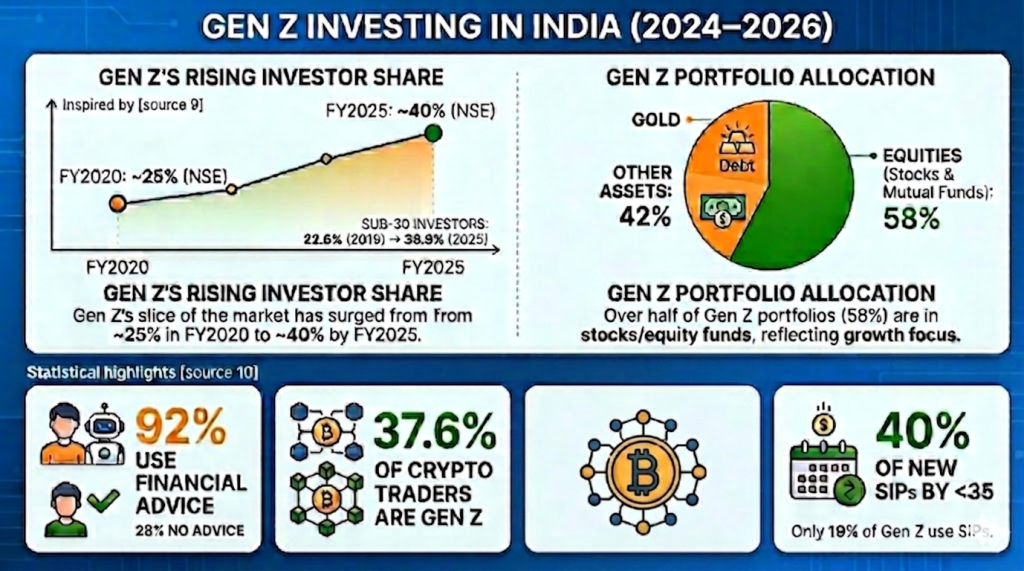

According to a report by NSE, over 56% of new mutual funds SIP registrations in India now come from investors under the age of 30. For the financial year 2024-25 (FY25), the NSE saw a 20.5% year-on-year increase in active demat accounts, with a significant portion of this growth driven by Gen Z and millennial investors

This isn’t accidental. Gen Z grew up with smartphones, survived the COVID-19 economic shock as teenagers, and watched their parents’ job security erode overnight. That experience made them hungry — not just for money, but for financial independence.

But early enthusiasm without a strategy is dangerous. That’s why Gen Z investing in India needs to go beyond Instagram reels and Reddit threads.

Gen Z Investing: What Makes This Generation Different?

Before diving into strategies, it’s important to understand what separates Gen Z investors from Millennials and older generations.

Digital-First by Default

Gen Z doesn’t visit bank branches. They open Zerodha accounts in 10 minutes, track SIPs on Groww, and discover stocks on Twitter (X) and YouTube. Their entire financial life happens on a 6-inch screen.

Risk-Aware but Not Risk-Averse

Contrary to what many assume, Gen Z in India isn’t afraid of risk — they’re afraid of uninformed risk.

Values-Driven Investing

ESG (Environmental, Social, and Governance) investing is no longer just a Western trend. Indian Gen Z investors are increasingly interested in green bonds, ESG mutual funds, and impact investing — aligning money with personal values.

Short Attention, Long Vision

Paradoxically, Gen Z thinks in both 10-second reels AND 10-year goals. They want quick onboarding and real-time data, but many are already thinking about FIRE (Financial Independence, Retire Early) in their 20s.

Top Investment Options for Gen Z in India (2026)

Here are the most viable and popular investment instruments available to Gen Z investors in India, ranked by accessibility and growth potential.

1. Mutual Funds via SIP (Systematic Investment Plan)

The most beginner-friendly option. Start with as little as ₹100/month on platforms like Groww, Zerodha Coin, or Paytm Money.

- Best for: Disciplined, long-term wealth creation

- Risk level: Low to High (depends on fund type)

- Expected return: 10–15% CAGR (equity funds, long term)

- Recommended fund categories: Flexi-cap, ELSS (tax-saving), Index funds

2. Direct Equity (Stocks)

Buying individual company shares on NSE/BSE. High reward, high risk — suitable for Gen Z who are willing to research.

- Best for: Those with time to track markets

- Platforms: Zerodha, Upstox, Angel One

- Risk level: High

- Pro tip: Start with blue-chip companies like Reliance Industries, Infosys, HDFC Bank before exploring mid/small caps

3.Index Funds & ETFs

Track market indices like Nifty 50 or Sensex. Lower cost than active funds. Warren Buffett’s recommended approach for most retail investors.

- Expense ratio: 0.05%–0.20% (extremely low)

- Best for: Passive investors who don’t want to pick stocks

- Popular options: Nifty 50 Index Fund, Nifty Next 50, Gold ETFs

4. Public Provident Fund (PPF)

A government-backed savings scheme with tax-free returns. Boring? Yes. But powerful for tax optimization.

- Interest rate: 7.1% p.a. (tax-free)

- Lock-in: 15 years

- Best for: The risk-free portion of a Gen Z portfolio

5. Digital Gold & Sovereign Gold Bonds (SGBs)

Gold has traditionally been India’s favorite asset. Gen Z is accessing it digitally.

- SGBs: Issued by RBI, offer 2.5% annual interest + gold price appreciation

- Digital Gold: Available on Paytm, PhonePe — buy in fractions

- Best for: Diversification and inflation hedge

6. REITs (Real Estate Investment Trusts)

Can’t afford a flat in Mumbai? Buy units of a REIT starting at ₹200–₹350.

- Examples: Embassy Office Parks REIT, Mindspace Business Parks REIT

- Returns: Quarterly dividends + NAV appreciation

- Best for: Exposure to real estate without massive capital

7. Cryptocurrency

High volatility, regulatory uncertainty in India, but undeniably present in Gen Z portfolios.

- Regulatory status: Taxed at 30% flat on gains (as per India’s crypto tax framework, in force since 2022)

- Platforms: CoinDCX, WazirX, CoinSwitch

- Recommendation: Limit to 5–10% of portfolio maximum

Step-by-Step: How to Start Investing as a Gen Z Indian

Follow this exact sequence to start your investment journey the right way:

Step 1: Build an Emergency Fund First Before investing a single rupee, save 3–6 months of expenses in a high-yield savings account or liquid fund. This is non-negotiable.

Step 2: Open a Demat + Trading Account You need a Demat account to hold shares and mutual funds. Top choices:

- Zerodha (best for active traders, flat ₹20/trade)

- Groww (best for beginners, zero brokerage on mutual funds)

- Upstox (competitive pricing, clean UI)

Step 3: Complete Your KYC India’s KYC process is now fully digital. You’ll need:

- Aadhaar card

- PAN card

- Bank account details

- A selfie + signature

Step 4: Start Small with a SIP Begin with ₹500–₹1,000/month in a Nifty 50 Index Fund. Let compounding do its work.

Step 5: Educate Yourself Continuously Follow credible sources: SEBI’s investor education portal, Freefincal, Zerodha Varsity, and The Financial Pandaa.

Step 6: Review Your Portfolio Every 6 Months Don’t obsessively check daily. Set a calendar reminder for a semi-annual portfolio review.

Step 7: Consult a Financial Advisor as You Scale Once your investable assets cross ₹5–10 lakh, bring in a qualified financial consultant or a certified financial planner (CFP) to guide your next phase of wealth building.

Financial Planner vs Financial Advisor vs Financial Consultant: What’s the Difference?

Many Gen Z investors use these terms interchangeably — but they mean very different things. Here’s a clear breakdown:

| Term | What They Do | Registration Required? | Ideal For |

| Financial Planner | Creates comprehensive life-stage financial plans (goals, insurance, tax) | CFP certification preferred | Long-term goal planning |

| Financial Advisor | Offers investment advice + portfolio management | CFP or relevant certifications preferred | Active portfolio management |

| Financial Consultant | Broad term — advises on financial products/solutions | Varies by specialization | One-time decisions, business finance |

| Wealth Manager | Holistic service for HNIs — portfolio + estate + tax | SEBI licensed | ₹50L+ investable assets |

Key Rule: Fee-Only vs Commission-Based

- Fee-only advisors charge you directly (₹5,000–₹25,000/year).

- Commission-based advisors earn from product sellers.

For Gen Z just starting out, a fee-only certified financial planner (CFP) is the most trustworthy option — they charge you directly and have no incentive to push products.

How to Verify a Financial Advisor’s Credentials in India

Before hiring any financial advisor, always ask for their CFP certification number, professional experience, and client references. Check if they are fee-only (paid by you) or commission-based (paid by product companies) — this distinction directly affects the quality and objectivity of advice you receive.

When Should Gen Z Hire a Financial Advisor in India?

Not everyone needs a financial advisor immediately. Here are clear signals that it’s time to hire one:

Hire a Financial Advisor When:

- Your annual income crosses ₹10 LPA and taxes are getting complex

- You receive a lump sum (inheritance, bonus, ESOP payout)

- You’re planning to buy property or take a home loan

- You’re getting married and need to combine finances

- Your investable corpus exceeds ₹10 lakh

- You’re starting a business and need wealth protection strategies

You Don’t Need an Advisor Yet If:

- You’re investing less than ₹10,000/month and just started

- Your portfolio is only index funds or simple SIPs

- You have no complex tax situation

The sweet spot for most Gen Z Indians: start self-directed, hire an advisor by age 28–32 or when financial complexity increases — whichever comes first.

Common Gen Z Investment Mistakes to Avoid

Even the most financially aware Gen Z investors fall into these traps:

Mistake 1: FOMO-Driven Investing

Buying a stock because it’s trending on Twitter. This is speculation, not investing. Stick to your thesis and time horizon.

Mistake 2:Ignoring Inflation

A savings account paying 4% when inflation is 6% means you’re losing money in real terms. Your investments must beat inflation consistently.

Mistake 3: No Asset Allocation Strategy

Going all-in on equities at 22 is fine — but having zero fixed-income allocation means you’ll panic-sell at the first market crash.

Recommended allocation for Gen Z (aggressive profile):

- Equities: 70–80%

- Debt/Fixed Income: 10–15%

- Gold/Alternative: 5–10%

- Emergency fund: separate

Mistake 4: Skipping Tax Planning

ELSS funds save ₹46,800/year in taxes under Section 80C under the old tax regime. NPS adds another ₹15,600 under Section 80CCD(1B). Not using these is leaving money on the table.

Mistake 5: Over-Diversification

Owning 15 mutual funds that all track similar indices = same risk, higher cost, no benefit. 3–5 well-chosen funds are better than 15 overlapping ones.

Mistake 6: Treating Crypto as a Core Investment

Crypto is speculative. It has no intrinsic cash flow, no regulatory safety net in India, and a 30% flat tax rate on gains. Treat it as a high-risk bet, not a retirement strategy.

The Role of Compounding: Why Starting at 22 Beats Starting at 32

This is the single most important concept for Gen Z investing.

Scenario A: Rohit starts investing ₹5,000/month at age 22, stops at 32 (10 years total).

Scenario B: Priya starts at 32 and invests ₹5,000/month until 60 (28 years total).

Assuming 12% CAGR:

| Total Invested | Portfolio at 60 | |

| Rohit (started at 22) | ₹6 lakh | ₹3.04 crore |

| Priya (started at 32) | ₹16.8 lakh | ₹1.76 crore |

Rohit invested less money and ended up with ₹1.28 crore more. That’s the compounding premium for starting early.

Summary

Key Takeaways for Gen Z Investing in India:

- Gen Z is the most active young investing cohort in Indian market history, driven by digital access and financial awareness

- Start with an emergency fund → open a Demat account → begin SIPs in index funds Best beginner instruments: Nifty 50 Index Funds, ELSS for tax savings, PPF for risk-free growth

- A financial planner focuses on life-stage goal planning; a financial advisor manages your portfolio; a financial consultant advises on specific decisions

- Hire a qualified financial advisor or certified financial planner (CFP) when your portfolio or income complexity increases significantly

- The biggest advantage Gen Z has is time — compounding rewards early starters disproportionately

- Avoid FOMO trading, over-diversification, crypto overexposure, and tax planning neglect

FAQ

1. What is the best investment for Gen Z in India with low risk?

For low-risk Gen Z investors in India, Public Provident Fund (PPF), Sovereign Gold Bonds (SGBs), and liquid mutual funds are the best options. They offer stable, inflation-beating returns with government backing. A PPF account can be opened at any post office or authorized bank with as little as ₹500/year.

2. At what age should a Gen Z Indian start investing?

The ideal age to start investing in India is as soon as you receive your first income — even if it’s an internship stipend. Starting at 21–22 vs 28–30 can mean a difference of crores in final corpus due to compounding. The minimum age for a Demat account in India is 18.

3. How much should Gen Z invest per month in India?

A practical rule of thumb is the 50-30-20 rule: 50% of income on needs, 30% on wants, 20% on savings/investments. Even ₹1,000–₹2,000/month in a SIP is an excellent starting point. As income grows, increase the SIP amount proportionally.

4. Do I need a financial advisor ifI’m just starting out?

No — you don’t need a financial advisor when you’re just starting small. Self-directed investing through index funds and SIPs is entirely manageable. Consider hiring a qualified financial advisor or certified financial planner (CFP) once your investable corpus exceeds ₹10 lakh or your financial situation becomes complex (tax, real estate, business).

5.Is cryptocurrency a good investment for Gen Z in India?

Cryptocurrency is highly speculative and taxed at 30% on gains in India with no loss offset benefit across assets. It can be a small part (5–10%) of a Gen Z portfolio, but should never be treated as a primary investment strategy. The regulatory environment in India for crypto remains evolving and uncertain.

6. What should I look for when choosing a financial advisor in India?

Look for a financial advisor who holds recognized certifications such as CFP (Certified Financial Planner) or CFA (Chartered Financial Analyst), has transparent fee structures (fee-only is preferred over commission-based), and has verifiable experience with clients in a similar financial situation as yours. Always ask upfront how they are compensated — this is the single most important question that reveals potential conflicts of interest.

7. What is the difference between a financial planner and a financial advisor in India?

A financial planner creates a comprehensive roadmap covering insurance, goals, tax, and estate planning — typically certified as a CFP (Certified Financial Planner). A financial advisor specifically manages investment portfolios and provides market-related guidance. Many professionals offer both services, but the titles carry distinct competency requirements and areas of focus.

8. How do I choose the best SIP for Gen Z in India?

For Gen Z, the best SIPs are typically: (1) Nifty 50 or Nifty Next 50 Index Funds for passive exposure, (2) Flexi-cap or multi-cap funds for diversified active management, and (3) ELSS funds for tax-saving under Section 80C under the old tax regime. Always check the fund’s 5-year CAGR, expense ratio (lower is better), and AUM before committing.