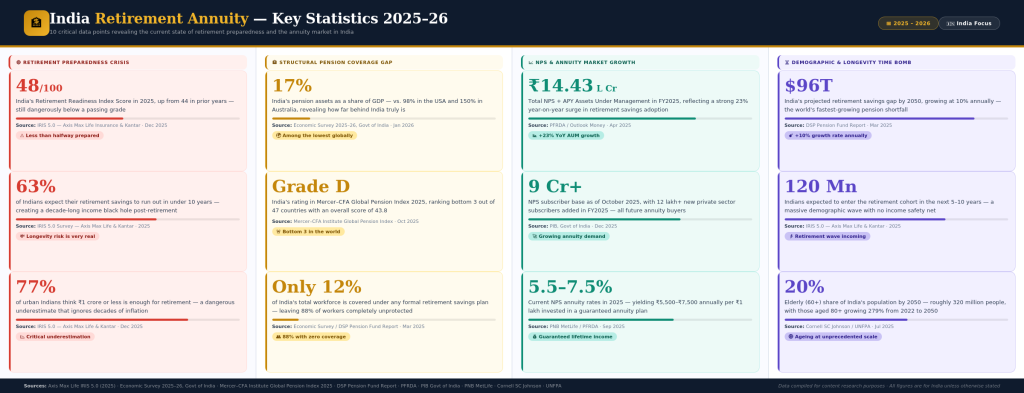

Retirement marks one of the most significant financial transitions in a person’s life. Yet, a large number of Indians approach it without a structured plan for sustaining income once their working years end. Savings accounts deplete, fixed deposit rates fluctuate, and the cost of living continues to climb. For those without an employer-provided pension, particularly self-employed individuals, private sector employees, and business owners, the absence of guaranteed income in retirement is a genuine concern.

This is where a retirement annuity becomes a relevant and practical solution. Offered by IRDAI-regulated insurance companies and structured under India’s broader pension framework, a retirement annuity provides a predictable income stream after retirement in exchange for contributions made during the working years. This guide covers what a retirement annuity is, how it works, what types are available, the applicable tax benefits, and how to choose the right product.

What Is a Retirement Annuity?

A retirement annuity is a contract between an individual and a registered financial institution (typically a life insurance company) under which the individual makes contributions, either as a lump sum or through regular payments, and the institution guarantees periodic income payments in return, either for a defined number of years or for the individual’s lifetime.

Two separate bodies regulate retirement annuity products in India depending on the product type:

- IRDAI (Insurance Regulatory and Development Authority of India) governs annuity plans offered by life insurance companies such as LIC, HDFC Life, SBI Life, and ICICI Prudential Life.

- PFRDA (Pension Fund Regulatory and Development Authority) governs the National Pension System (NPS), which includes a mandatory annuity component at the time of retirement.

A common point of confusion is the difference between a pension and an annuity. The employer funds and administers a pension, such as the one provided to government employees under the old pension scheme. A retirement annuity, by contrast, is a product that individuals purchase independently, either through an insurer or through NPS, giving them full control over how much they contribute and when payouts begin.

How Does a Retirement Annuity Work?

A retirement annuity operates through a clear, step-by-step process, starting from the moment you select a plan and continuing well into retirement:

- Plan Selection: The individual selects a retirement annuity plan from a registered insurer or opts into NPS through a Point of Presence (PoP) such as a bank or post office.

- Contribution Phase: Regular premiums or contributions are made. These can be monthly, quarterly, annual, or a one-time lump sum depending on the plan type.

- Accumulation Phase: Contributions grow over time, either at a fixed guaranteed rate (in traditional plans) or linked to market performance (in unit-linked or NPS-based plans).

- Vesting / Retirement Trigger: At the chosen vesting age or retirement date, the payout phase is activated.

- Annuity Purchase (for NPS): NPS subscribers must use at least 40% of their accumulated corpus to purchase an annuity from an IRDAI-registered annuity service provider at the time of exit.

- Distribution Phase: Regular income payments begin: monthly, quarterly, or annually, and continue for the agreed period or for life.

Types of Retirement Annuity Products Available in India

India’s retirement landscape offers several distinct products under the broad umbrella of the retirement annuity. Each serves a different need:

| Product Type | How It Works | Regulated By | Best Suited For |

| Immediate Annuity Plan | A lump sum is paid to the insurer; payouts begin almost immediately. | IRDAI | Retirees who need income right away |

| Deferred Annuity Plan | Contributions are made over time; payouts begin at a future vesting date | IRDAI | Working individuals building a retirement corpus |

| Unit-Linked Pension Plan (ULPP) | Market-linked returns during accumulation; annuity at vesting. | IRDAI | Those comfortable with market exposure for higher growth |

| National Pension System (NPS) | Contributions invested across equity, corporate bonds, and government securities; 40% must be used to buy an annuity at exit | PFRDA | Salaried employees, self-employed individuals seeking flexibility and tax efficiency |

| Atal Pension Yojana (APY) | Fixed guaranteed pension of ₹1,000–₹5,000/month at age 60, based on contributions | PFRDA | Informal sector workers and low-income earners |

Each product carries a different risk-return profile and regulatory structure. A qualified financial consultant can assess individual circumstances and recommend the most suitable option before you make any commitment.

Tax Benefits of a Retirement Annuity in India

Tax treatment is one of the most important factors to evaluate when selecting a retirement annuity product in India. The applicable sections differ depending on the product chosen and the tax regime opted for.

For IRDAI-Regulated Annuity and Pension Plans (Section 80CCC)

Premiums paid toward annuity or pension plans from insurance companies are eligible for tax deductions under Section 80CCC of the Income Tax Act, 1961, up to ₹1.5 lakh per financial year. This deduction falls within the overall ₹1.5 lakh ceiling shared with Section 80C.

It is important to note that the new tax regime removes the 80C/80CCC deduction benefit entirely, which changes the value proposition for many buyers. Those opting for the new tax regime cannot claim deductions on annuity premiums paid to insurance companies.

For NPS (Sections 80CCD(1), 80CCD(1B), and 80CCD(2))

| Section | Benefit | Old Tax Regime | New Tax Regime |

| 80CCD(1) | Deduction on self-contributions to NPS: up to 10% of salary for salaried, 20% of gross income for self-employed | Available | Not available |

| 80CCD(1B) | Additional deduction of up to ₹50,000 over and above the 80C limit | Available | Not available |

| 80CCD(2) | Deduction on employer’s NPS contribution: up to 14% of salary (basic + DA) | Available | Available |

If a taxpayer opts for the new regime, they cannot claim deductions under Section 80CCD(1) and 80CCD(1B). However, they can still claim employer contributions under Section 80CCD(2).

At the Time of Withdrawal (NPS)

Under the old tax regime, a retiree can withdraw up to 60% of the total accumulated NPS corpus as a lump sum at retirement, and this withdrawal remains tax-exempt. The remaining 40% is required to be used for purchasing an annuity plan, and the amount utilised to purchase the annuity is also exempt from tax at the time of purchase. However, the annuity income received thereafter is taxable as per the individual’s applicable income tax slab in the year of receipt.

Overall, the old tax regime offers significantly more tax advantages for retirement annuity products, particularly for NPS contributors. Those in the new tax regime benefit primarily through the employer contribution deduction under Section 80CCD(2). Consulting a financial consultant before deciding which regime to opt for is strongly advisable.

Key Benefits of a Retirement Annuity

- Guaranteed Lifetime Income: Fixed annuity plans from IRDAI-regulated insurers provide income that continues regardless of market conditions, addressing the risk of outliving one’s savings.

- Tax Efficiency: Contributions attract meaningful deductions under Sections 80CCC and 80CCD, reducing taxable income during the working years (under the old tax regime).

- Flexible Payout Options: Plans offer monthly, quarterly, half-yearly, or annual payout frequencies.

- Joint Life Options: Many plans include a joint-life annuity option, ensuring that a surviving spouse continues to receive income after the primary annuitant’s death.

- Return of Purchase Price: Several plans, including those from LIC and HDFC Life, offer the option to return the original premium paid to the nominee upon the annuitant’s death.

- Inflation-Linked Options: Certain indexed annuity variants offer increasing payouts to partially offset inflation over time.

Professional retirement planning services can help individuals identify the combination of these features that best aligns with their income requirements and family situation.

Potential Drawbacks to Consider

- Illiquidity: Once a traditional annuity plan is purchased, early exit is heavily restricted and may attract surrender penalties.

- Taxable Annuity Income: Unlike certain other instruments such as PPF, annuity payouts are fully taxable as income in the year of receipt, regardless of the tax regime.

- Inflation Risk in Fixed Plans: A fixed monthly payout that seems adequate at 60 may lose purchasing power significantly by age 75 or 80, given India’s average inflation rate.

- Complexity of NPS Annuity Selection: At the time of NPS exit, subscribers must choose an annuity provider from a panel of IRDAI-registered insurers, a decision that requires careful comparison of payout rates, joint-life options, and provider stability.

- New Tax Regime Disadvantage: Those who have opted for the new tax regime lose access to most contribution-related deductions, reducing the tax efficiency of the product.

- Provider Dependency Annuity payouts depend on the continued solvency of the issuing insurer. If a company fails, IRDAI steps in to transfer the policy to another insurer, and payouts may pause briefly but will not stop permanently.

Who Should Consider a Retirement Annuity in India?

Apart from individuals like private sector employees, self-employed professionals, or business owners, who have no employer-funded retirement benefit and rely entirely on personal savings for retirement income, retirement annuity is also particularly relevant for the following individuals:

- Individuals who want a source of income that does not depend on stock market performance

- Conservative investors who prioritise financial security over the potential for high returns

- NPS subscribers who want to plan the mandatory 40% annuity purchase strategically before reaching retirement age

- Those who have already exhausted their Section 80C limit and are looking for additional tax-efficient retirement savings through Section 80CCD(1B)

How to Choose the Right Retirement Annuity in India

- Define Monthly Income Requirements: Estimate the amount needed per month to cover living expenses, healthcare, and other costs during retirement, factoring in inflation.

- Compare Products Across Regulators: Evaluate both IRDAI-regulated plans (traditional and unit-linked pension plans) and PFRDA-governed NPS options side by side, rather than defaulting to one without comparison.

- Assess Tax Regime Compatibility: Determine whether the old or new tax regime is more beneficial for overall tax liability, as this directly affects how much value a retirement annuity delivers in terms of deductions.

- Compare Annuity Rates Across Providers: For immediate annuities and NPS annuity purchases, request written quotes from multiple registered providers and compare actual monthly payout figures rather than relying on online calculators alone.

- Examine Plan Features: Look closely at joint-life options, return of purchase price provisions, inflation-linkage features, and guaranteed minimum payout periods before selecting a plan.

- Engage Professional Guidance: Work with trusted retirement plan services to model different contribution levels, retirement ages, and product combinations to identify the option that delivers the most suitable outcome.

- Review Periodically: Income needs, tax laws, and product availability change over time. Reviewing the retirement plan every three to five years ensures it remains aligned with current circumstances.

Conclusion

A retirement annuity remains one of the most reliable instruments available for building a dependable, structured income after retirement in India. Whether through an IRDAI-regulated insurance plan, the NPS framework, or a combination of both, these products address a fundamental challenge — sustaining consistent income in a phase of life when active earnings have ended.

The decision to invest in a retirement annuity should be made with a clear understanding of the available product types, applicable tax provisions under both the old and new tax regimes, and the specific income needs of the individual. Given the complexity involved, particularly around NPS annuity selection, tax regime comparison, and provider evaluation, the guidance of a certified financial consultant is not just helpful but often essential.

Retirement security in India does not arrive automatically. It is built through deliberate, well-informed decisions, and the earlier those decisions are made, the more time a retirement annuity has to work in the individual’s favour.

Disclaimer: The information in this article is for informational purposes only and does not constitute financial advice. Tax provisions and regulatory guidelines referenced are based on publicly available information as of May 2026 and are subject to change. Please consult a certified financial consultant or tax adviser before making any investment decisions.