WHY RETIREMENT PLANNING MATTERS FOR SELF-EMPLOYED PROFESSIONALS

As a self-employed individual—whether you’re a freelancer, consultant, small business owner, or entrepreneur—you face a unique financial reality. Finding the right retirement plans for self-employed professionals is critical because unlike salaried employees, you won’t have employer-sponsored retirement contributions.

The numbers tell the story:

- The average Indian retiree needs ₹25-30 lakhs to live comfortably for 20-25 years (assuming 5% annual inflation)

- Self-employed income is often inconsistent, making retirement savings challenging

But here’s the good news: India’s government has created multiple retirement plan options specifically designed for self-employed professionals. These plans offer tax advantages, flexible contributions, and reasonable returns.

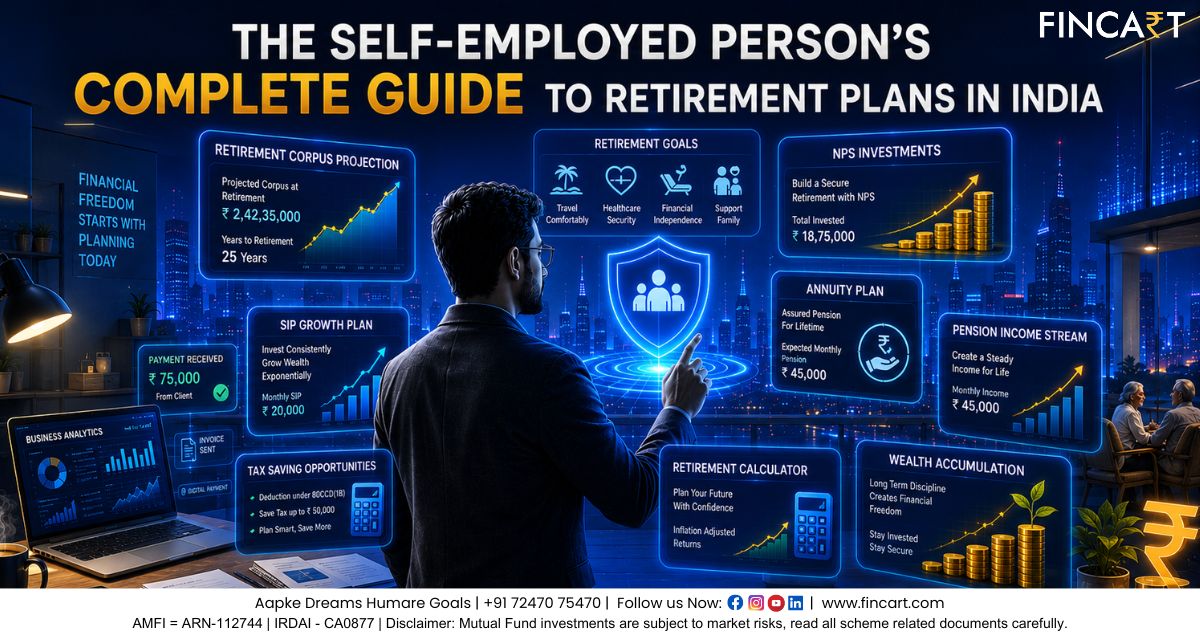

The real impact: A 35-year-old self-employed professional who invests ₹50,000 annually in an NPS account for 30 years can accumulate ₹1+ crore at 8% returns.

TOP RETIREMENT PLAN OPTIONS FOR SELF-EMPLOYED IN INDIA

Let’s explore the major retirement plan services available in India. When evaluating retirement plans for self employed professionals, you’ll find several government-backed and private options designed specifically for your needs.Understanding the different retirement plans for self-employed is critical because each offers unique benefits, tax advantages, and withdrawal flexibility. Here are the main options:

1. National Pension System (NPS) – Tier I & Tier II

Regulated by the Pension Fund Regulatory and Development Authority (PFRDA), this is India’s most flexible government-backed retirement plan.

2. Pradhan Mantri Vaya Vandana Yojana (PMVVY)

A guaranteed pension scheme offering fixed monthly income after retirement.

3. Atal Pension Yojana (APY)

An affordable, government-guaranteed pension plan for low-income earners.

4. Private Insurance Annuity Plans

Life insurance companies offering retirement annuities with flexible payout options.

5. Senior Citizen Savings Scheme (SCSS)

A fixed-income investment option for individuals above 60 years.

6. Bank Fixed Deposits & Post Office Schemes

Conservative options with guaranteed returns and partial liquidity.

Each option has distinct advantages. Let’s dive deeper into the best choices for self-employed retirement planning.

NATIONAL PENSION SYSTEM (NPS): THE GOVERNMENT-BACKED CHOICE

What is NPS?

The National Pension System is a voluntary, market-linked retirement investment scheme launched in 2004. It’s managed by the PFRDA and is the most widely used retirement plan services platform in India—and arguably the best retirement plan for self-employed professionals seeking both growth and tax benefits.

Think of NPS as a personalized retirement investment account where you control both contributions and investment choices.

How NPS Works for Self-Employed Professionals

Step-by-step breakdown:

- Open an account with an NPS nodal agency (banks, post offices, or PFRDA-registered intermediaries)

- Choose your investment mix – from conservative to aggressive equity allocations

- Make contributions – as per your financial capacity (₹500-50,000+ per year)

- Accumulate wealth over 30-40 years through market growth

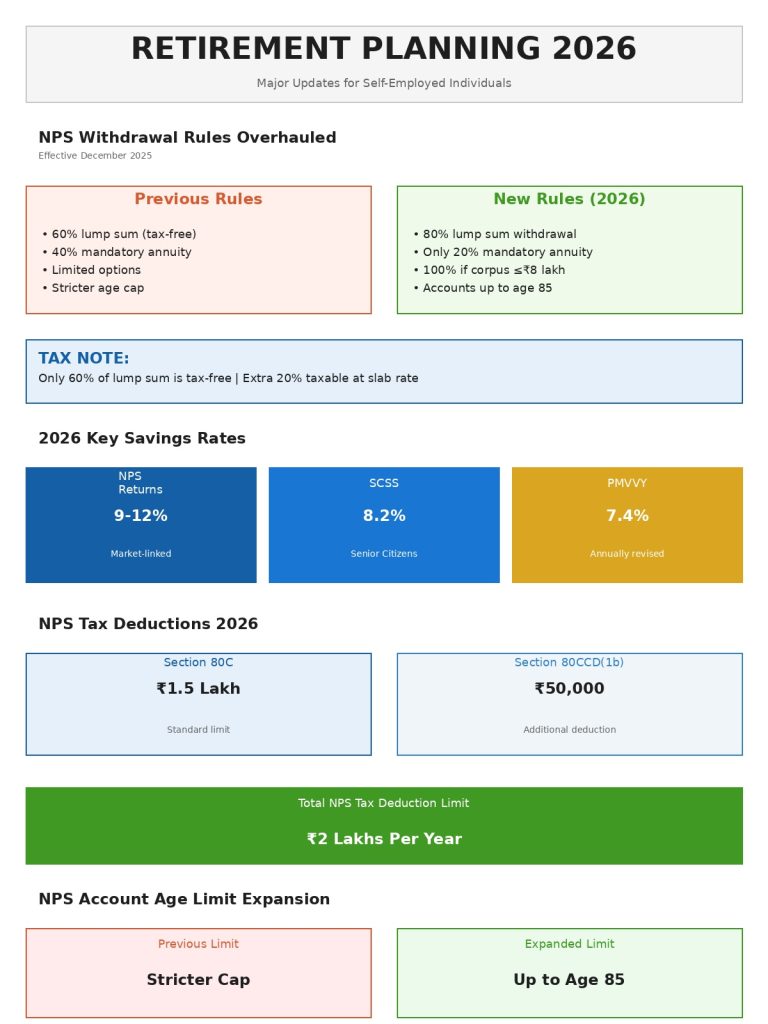

- At retirement – withdraw up to 80% as lump sum and purchase an annuity with remaining 20% (effective 2026)

NPS Investment Options Explained

| Allocation Type | Risk Level | Recommended For | Average Returns (10-year, 2026) |

| Government Securities (G) | Very Low | Conservative investors | 5.5-6.5% |

| Corporate Bonds (C) | Low-Medium | Balanced approach | 6.5-7.5% |

| Equity (E) | High | Long-term investors (15+ years) | 9-12% |

| Hybrid (H) | Medium | Most self-employed professionals | 7.5-9.5% |

Tax Benefits of NPS for Self-Employed

This is where NPS shines for retirement planning:

- Section 80C deduction: Contributions up to ₹1.5 lakhs per financial year reduce your taxable income

- Section 80CCD(1b) additional benefit: An extra ₹50,000 deduction for NPS contributions above the ₹1.5 lakh limit

- Tax-free growth: Investment returns aren’t taxed annually

- Low contribution fees: Only ₹100-200 annual subscription charge

Real example: A self-employed professional earning ₹50 lakhs annually:

- Invests ₹2 lakhs in NPS yearly

- Gets tax deduction of ₹2 lakhs

- At 30% income tax rate, saves ₹60,000 in taxes

- Over 15 years: ₹9 lakhs in tax savings + investment growth

Liquidity & Withdrawal Rules (Updated 2026)

Major NPS Withdrawal Reform (Effective December 2025):

Non-government NPS subscribers now enjoy significantly more flexibility:

| Scenario | Amount Allowed | Tax Status | Annuity Requirement |

| Corpus ≤ ₹5 lakh | |||

| Corpus ₹5-₹8 lakh | |||

| Corpus ₹8-₹12 lakh | |||

| Corpus > ₹12 lakh | |||

| Government employees |

Important 2026 Tax Note: While you can withdraw 80% as lump sum, only 60% is tax-free under Section 10(12A). The additional 20% withdrawal is taxable at your income slab rate.

PRADHAN MANTRI VAYA VANDANA YOJANA (PMVVY): GUARANTEED INCOME

Who Should Choose PMVVY?

PMVVY is ideal if you value guaranteed returns over market-linked growth and want a defined pension for life.

Key Features of PMVVY (2026 Update)

- Guaranteed pension: 7.4% per annum (currently; rates now revised annually)

- Monthly income: ₹775 per month for every ₹1 lakh invested (at 7.4%)

- Investment period: 10 years

- Maximum investment: ₹15 lakhs per person

- Eligibility: Indian citizens aged 60+ years

- Interest rate revision: Effective 2026, rates are now disclosed and revised annually (previously fixed for full tenure)

How PMVVY Works

You make a lump-sum investment and receive a guaranteed monthly pension starting from the first month of investment; the policy term is 10 years, after which the principal is returned to the investor.

Example: A 60-year-old self-employed person invests ₹10 lakhs in PMVVY at current 7.4%.

- Monthly pension = ₹7,750

- Annual pension = ₹93,000

- This continues for life, transferring to spouse if needed

2026 Note: The annual rate revision means rates may change after the tenure period, but pension for the existing contract remains locked.

PMVVY vs. NPS: Key Differences (2026)

| Feature | PMVVY | NPS |

| Returns | Fixed 7.4% (reviewed annually) | Market-linked (9-12%, 2026) |

| Flexibility | Limited – 10-year lock-in | Can exit after 15 years; access after 7 years with restrictions |

| Risk | None (government-backed) | Market risk involved |

| Withdrawal | Only in exceptional cases | 80% lump sum now (2026 rules) |

| Tax benefit | Partial (interest taxable) | Full 80C deduction + extra 50K under 80CCD(1b) |

| Best for | Risk-averse older investors | Long-term wealth builders (age 18-85) |

ATAL PENSION YOJANA (APY): THE AFFORDABLE OPTION

What Makes APY Different?

APY is the most inclusive retirement plan services option, designed for workers in the unorganized sector and low-income self-employed professionals.

APY Features

- Flexible contribution: ₹84 to ₹1,454 monthly (₹1,000-17,500 annually)

- Guaranteed pension: ₹1,000 to ₹5,000 per month based on contribution

- Government co-contribution: 50% match for early subscribers (until 2015 for eligible)

- Enrollment: Ages 18-40 for best benefits

How Much Pension Will You Get?

| Target Monthly Pension | Contribution at Age 25 | Contribution at Age 35 |

| ₹1,000/month | ₹84/month | ₹291/month |

| ₹2,000/month | ₹168/month | ₹582/month |

| ₹5,000/month | ₹420/month | ₹1,454/month |

All contributions are tax-deductible, and the pension is guaranteed.

PRIVATE INSURANCE PLANS: FLEXIBILITY & COVERAGE

Understanding Insurance-Based Retirement Plans

Major insurance companies (LIC, HDFC, ICICI, Bajaj) offer retirement annuity plans that combine life insurance with pension benefits.

How These Plans Work

- Pay premiums during the earning years

- At retirement, the insurance company converts your accumulated fund into a guaranteed pension for life

- Coverage includes death benefit if you pass away before retirement

Types of Insurance Retirement Plans

Immediate Annuity Plans:

- You invest a lump sum at age 55-60

- Receive pension immediately for life

- Best for people with accumulated savings

Deferred Annuity Plans:

- Pay premiums over 20-30 years

- Receive pension after retirement

- Lower premium, higher pension

Tax Benefits of Insurance Plans

- Premiums qualify for Section 80C deduction (up to ₹1.5 lakhs)

- Growth inside the policy is tax-free

- Pension income received is taxable as per your income slab

Comparison with NPS: NPS offers higher tax deductions (up to ₹2 lakhs with 80CCD(1b)), while insurance plans provide additional life cover during the accumulation phase.

COMPARISON TABLE: WHICH PLAN SUITS YOU?

Choosing among various retirement plans for self employed can be confusing. This comparison table helps you evaluate the best retirement plans for self-employed based on your needs, income level, and risk tolerance.

| Criteria | NPS | PMVVY | APY | Insurance Plan |

| Min. Monthly Contribution | ₹500/year | ₹10,000/month (lump sum) | ₹84/month | ₹1,000-5,000/month |

| Maximum Returns | 12%+ | 7.4% fixed | 8-9% | 6-8% |

| Liquidity | Good (after 7 years) | Poor (10-year lock-in) | Locked till 60 | Limited |

| Market Risk | Yes | No | No | No |

| Tax Deduction | ₹2 lakhs | Partial | Partial | ₹1.5 lakhs |

| Life Insurance | No | No | No | Yes |

| Best For | Long-term builders | Risk-averse retirees | Low-income workers | Comprehensive coverage |

TAX BENEFITS: HOW MUCH CAN YOU SAVE?

As a self-employed professional, retirement contributions can significantly reduce your tax liability.

Tax Deduction Breakdown for FY 2024-25

Primary deduction (Section 80C):

- Contributions to NPS, insurance, EPF = up to ₹1.5 lakhs deduction

- Applies to all retirement plans

Additional NPS deduction (Section 80CCD(1b)):

- Extra ₹50,000 deduction for NPS contributions above ₹1.5 lakhs

- Maximum total NPS deduction = ₹2 lakhs

HRA/Medical Insurance deductions:

- Section 80D: Up to ₹1 lakh for health insurance premiums

- Additional ₹50,000 for parents’ health insurance

Real Tax Saving Example

Scenario: Self-employed earning ₹60 lakhs annually (30% tax bracket)

Without retirement planning:

- Taxable income = ₹60 lakhs

- Tax due = ₹18 lakhs

With strategic retirement planning:

- NPS contribution = ₹2 lakhs

- Health insurance premium = ₹50,000

- Total deductions = ₹2.5 lakhs

- Taxable income = ₹57.5 lakhs

- Tax due = ₹17.25 lakhs

- Annual tax savings = ₹75,000

Over 25 years: ₹18.75 lakhs saved in taxes, plus investment growth.

STEP-BY-STEP GUIDE: SETTING UP YOUR RETIREMENT PLAN

Opening a retirement plan might seem daunting, but it’s easier than you think. If you’ve decided NPS is the right choice among all retirement plans for self employed, here’s exactly how to set up your account:

How to Open an NPS Account (Best for Most Self-Employed)

Choose Your NPS Service Provider

- HDFC Bank, ICICI Bank, AXIS Bank (banks)

- India Post (convenient for rural areas)

- PFRDA-registered financial advisors

Gather Required Documents

- PAN card (mandatory)

- Aadhaar card (for eKYC)

- Recent address proof

- Bank account details

Complete the Application

- Fill Form A (account opening form)

- Complete eKYC (online verification)

- Submit documents (in-person or online, depending on provider)

Activate Your Account

- You’ll receive a Permanent Retirement Account Number (PRAN)

- Access your account via NSDL eGovernance portal

- Takes 5-7 working days

Set Up Contributions

- Link your bank account for auto-debit

- Choose investment option (conservative/balanced/aggressive)

- Decide contribution frequency (monthly/quarterly/annual)

Monitor & Rebalance

- Review portfolio performance quarterly

- Rebalance allocation as you age (shift from equity to bonds)

- Increase contributions annually with income growth

Alternative: Opening PMVVY Account

- Receive guaranteed pension starting at age 60

- Visit your nearest post office or authorized bank

- Provide KYC documents (Aadhaar, PAN, address proof)

- Complete PMVVY application form

- Deposit minimum ₹1.5 lakhs

- Receive certificate of investment

COMMON MISTAKES TO AVOID

Mistake 1: Starting Too Late

The problem: A 45-year-old with 20 years to retirement needs to invest ₹12,000 monthly to accumulate ₹30 lakhs. A 30-year-old needs only ₹3,500 monthly for the same goal.

The solution: Start immediately, even with small amounts (₹1,000-2,000 monthly).

Mistake 2: Chasing High Returns and Taking Unnecessary Risk

The problem: Allocating 100% to equities at age 55 can mean devastating losses near retirement.

The solution: Follow the “100-minus-age” rule. If you’re 50, allocate 50% to equities, 50% to bonds.

Mistake 3: Not Diversifying Across Plans

The problem: Putting all savings in NPS means market risk concentration.

The solution: Combine NPS (growth) + insurance (stability) + SCSS (fixed income) for balanced retirement.

Mistake 4: Ignoring Inflation

The problem: ₹30 lakhs today might be worth ₹15 lakhs in 25 years due to inflation.

The solution: Increase contributions by 10-15% annually and maintain equity allocation.

Mistake 5: Not Reviewing Tax Strategy

The problem: Missing deduction opportunities = paying unnecessary taxes.

The solution: Consult a CA annually to optimize Section 80C, 80CCD, 80D deductions.

Mistake 6: Overlooking Life Insurance

The problem: If you die at 55, NPS corpus goes to heirs (good), but you wanted monthly income for your family (not guaranteed).

The solution: Pair NPS with a term life insurance policy to cover your family’s living expenses.

QUICK SUMMARY FOR BUSY SELF-EMPLOYED PROFESSIONALS

Can’t decide which among the many retirement plans for self employed is right for you? This quick reference guide helps you match your financial goals with the best retirement plan option:

| If You Want… | Best Plan | Monthly Contribution | Expected at 60 |

| Maximum tax benefit + growth | NPS (Hybrid) | ₹8,000-15,000 | ₹1-2 crore |

| Guaranteed fixed income | PMVVY | ₹1,50,000 – ₹15,00,000 (one-time lump sum) | ₹7,750/month for life |

| Affordable pension + govt support | APY | ₹500-1,200 | ₹1,000-5,000/month |

| Comprehensive protection | Insurance Annuity | ₹5,000-10,000 | ₹40,000-80,000/month + death cover |

| Conservative, liquid savings | SCSS or Bank FDs | Variable | 8.2% SCSS (guaranteed) |

FREQUENTLY ASKED QUESTIONS {#faq}

1. Can I contribute to multiple retirement plans simultaneously?

Yes, absolutely. The smartest self-employed professionals use a multi-plan approach:

- Primary: NPS for maximum tax deduction and growth

- Secondary: PMVVY or insurance plan for income guarantee

- Tertiary: SCSS or bank FDs for stability

The government doesn’t restrict plan combinations—only the total 80C deduction is capped at ₹1.5 lakhs (plus additional ₹50,000 for NPS alone).

2. What happens to my NPS account if I die before retirement?

Your entire accumulated corpus goes to your legal heirs—no loss. This makes NPS superior to some insurance plans for wealth transfer.

However, your family won’t receive monthly pension unless you had also purchased a life insurance plan.

3. Is NPS better than EPF for self-employed?

Important note: EPF is only for formal sector employees. Self-employed professionals cannot access EPF unless they register as an employer and employ others.

Instead, self-employed professionals should use NPS, which offers similar or better tax benefits without the strict withdrawal rules of EPF.

4. Can I withdraw from NPS before 60 years of age?

Pre-retirement withdrawal (Before 60):

- After 7 years of contribution: Can withdraw up to 50% of accumulated corpus OR 50% of last 4 years’ contributions, whichever is lower

- Permitted only for specified purposes: higher education of children, marriage of children, purchase/construction of house, critical illness treatment

At retirement (60 years and above) – Updated 2026 Rules:

For non-government subscribers (most self-employed):

- Corpus ≤ ₹8 lakh: Withdraw 100% as tax-free lump sum (no annuity required)

- Corpus ₹8-₹12 lakh: Withdraw ₹6 lakh lump sum + remaining through Systematic Unit Redemption (SUR)

- Corpus > ₹12 lakh: Withdraw up to 80% as lump sum (60% tax-free, 20% taxable at slab rate) + mandatory 20% in annuity

For government employees: Remain at 60% lump sum, 40% annuity

This is a significant improvement from the older 60% lump sum / 40% annuity rule.

5. How much should I contribute monthly for a comfortable retirement?

Use the 50-70% rule: Your monthly pension should be 50-70% of your current monthly expenses.

Calculation method:

- Current monthly expenses: ₹1,00,000

- Target retirement income: ₹60,000-70,000 (adjusted for inflation)

- Use a retirement calculator on PFRDA website to determine required monthly contribution

General guideline: Invest 15-20% of your income in retirement plans.

A ₹50-lakh-earning professional should invest ₹7,500-10,000 monthly across all plans.

6. Are retirement plan returns guaranteed?

Depends on the plan (2026 data):

- NPS: Market-linked—returns fluctuate (currently 9-12% p.a. as of 2026)

- PMVVY: Fixed 7.4% annual returns—completely guaranteed

- APY: Guaranteed pension amount (government-backed)

- SCSS: 8.2% per annum (as of June 2026, unchanged since April 2024)

- Insurance annuities: Guaranteed pension with participation in bonus

Hybrid approach: Combine NPS (growth) with PMVVY/SCSS (safety) to balance risk and returns.

7. Can I switch my NPS investment allocation as I age?

Yes, with unlimited switches annually. This is crucial.

Recommended strategy:

- Age 25-40: 80% equities, 20% bonds

- Age 40-50: 60% equities, 40% bonds

- Age 50-60: 40% equities, 60% bonds

- Age 60+: 20% equities, 80% bonds

Each switch is free, and you can rebalance quarterly online.

8. What if I cannot contribute consistently due to irregular income?

NPS allows flexible contributions:

- Minimum: As low as ₹500 annually

- No fixed schedule—contribute whenever possible

- Even ₹5,000 annually (₹417/month) creates long-term wealth

Self-employed with irregular income should contribute when revenue is strong and skip months when revenue is low—NPS allows this flexibility.