Freelancing has become one of the most popular career choices in India. Writers, designers, developers, consultants, and marketers are all building independent careers and earning solid incomes without a traditional employer. But with that freedom comes a responsibility freelancers might overlook: paying tax correctly. Understanding freelancer income tax in India is not optional. It is a legal requirement, and getting it wrong can lead to penalties, interest charges, and unwanted attention from the tax department.

This guide breaks down everything a freelancer in India needs to know about filing income tax in 2026.

Why Freelancer Income Tax in India Works Differently

When you work for a company as an employee, your employer deducts tax at source and hands you a Form 16 at the end of the year. As a freelancer, there is no employer doing this for you. Your income is treated as “income from business or profession,” not salary. This single difference changes everything about how you calculate, report, and pay tax.

Freelancer income tax in India applies the moment your total income for the financial year crosses the basic exemption limit. It does not matter whether your clients are in Mumbai or in New York. If you are a tax resident of India, your worldwide freelance income is taxable here, including payments received through freelance platforms.

Step 1: Know Your Income Tax Slabs for FY 2025-26

The biggest update affecting freelancer income tax in India this year is the new tax regime. It remains the default system for all taxpayers, including those earning through business or profession, under Section 115BAC. The Union Budget 2026 made no changes to these slabs, so the rates that applied for FY 2025-26 continue into FY 2026-27 as well.

New Tax Regime slabs (FY 2025-26, AY 2026-27):

| Income Range | Tax Rate |

| Up to ₹4 lakh | Nil |

| ₹4 lakh to ₹8 lakh | 5% |

| ₹8 lakh to ₹12 lakh | 10% |

| ₹12 lakh to ₹16 lakh | 15% |

| ₹16 lakh to ₹20 lakh | 20% |

| ₹20 lakh to ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

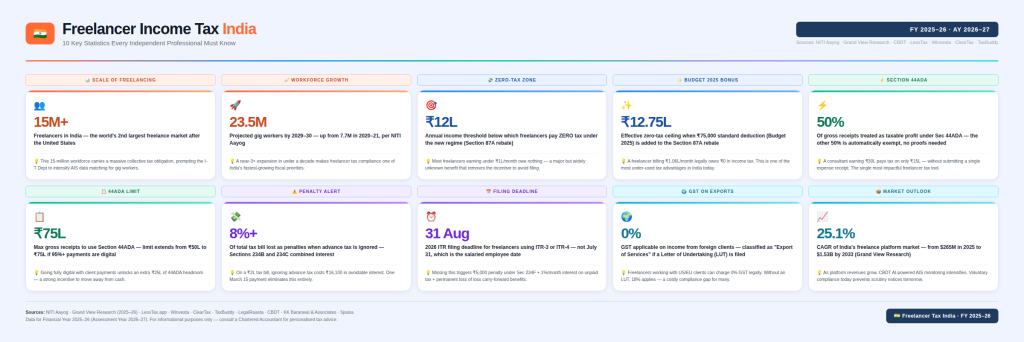

Thanks to the Section 87A rebate, income up to ₹4 lakh is tax-free, and the highest rate of 30% only applies above ₹24 lakh. This rebate effectively means freelancers with taxable income up to ₹12 lakh under the new regime can end up paying zero tax, which is a major relief for early-career freelancers and small consultants.

Old Tax Regime:

This option still exists if you prefer to claim deductions like 80C investments, 80D health insurance premiums, and home loan interest. Under the old regime, income up to ₹2.5 lakh is tax-free, and tax starts at 5% between ₹2.5 lakh and ₹5 lakh, rising through the usual slabs to 30% for income above ₹10 lakh. If you have heavy investments or deductions to claim, the old regime might still work out cheaper, so it is worth comparing both before filing.

Step 2: Choose How You Want to Calculate Your Profit

As a freelancer, tax does not apply to everything you earn. It applies to your profit, which is your total receipts minus the money you spend to do your work. The government gives you two ways to calculate this profit. Which method works for you depends on your profession, your annual earnings, and how high your real expenses are.

Option A: Presumptive Taxation under Section 44ADA

Section 44ADA lets specified professionals declare 50% of their gross receipts as taxable profit, regardless of what they actually spent on expenses. This means:

- You do not need to maintain detailed books of accounts.

- You do not need a tax audit, even if your income is substantial.

- You pay tax on half your earnings and move on.

Eligibility for Section 44ADA:

- You must be in a specified profession, such as legal, medical, engineering, architecture, accountancy, technical consultancy, interior decoration, or similar professional and creative freelance work.

- Your annual gross receipts must not exceed ₹50 lakh, or ₹75 lakh if less than 5% of your total receipts are in cash.

- You must declare at least 50% of receipts as profit. Declaring lower and still using this scheme is not permitted.

Consider an example: Ravi is a freelance interior decorator earning ₹30 lakh in receipts during the year. His actual expenses, including rent, phone bills, and travel, come to ₹10 lakh. Instead of calculating his real profit, Ravi opts for Section 44ADA and declares ₹15 lakh (50% of ₹30 lakh) as his taxable income. This saves him from maintaining detailed books and simplifies his return considerably.

Option B: Filing Income Tax on Actual Profits (ITR-3)

If your actual expenses exceed 50% of your receipts, or if your gross receipts cross the ₹75 lakh limit, you must move to the regular method. Here, you calculate your real profit by subtracting genuine business expenses from your gross receipts. These can include software subscriptions, internet bills, a portion of rent for a home office, and marketing costs. This route requires maintaining proper books of accounts, and if your receipts exceed certain thresholds, a tax audit becomes mandatory.

Consider an example: Priya is a software developer with ₹80 lakh in gross receipts, split between ₹40 lakh from foreign clients on Upwork and ₹40 lakh from Indian clients. Her real expenses total ₹45 lakh, covering software tools, a home office, internet, marketing, travel, and accounting fees. Because her receipts exceed the ₹75 lakh presumptive limit, Priya must file under ITR-3, maintain proper books, and get her accounts audited.

Step 3: Handling Foreign Client Income

A growing share of Indian freelancers work with international clients, and freelancer income tax in India applies fully to this income too, since Indian residents are taxed on their global earnings. To handle it correctly:

- Convert to INR: Use the bank’s exchange rate on the date the payment lands in your account, and report the full amount before any platform deducts its service fees.

- Pick your calculation method: Apply Section 44ADA if you qualify, or calculate actual profit and file ITR-3 if your receipts are higher or expenses exceed 50%.

- Apply the tax slabs: Use either the new or old regime rates on your final taxable income, after subtracting any eligible deductions.

- Claim relief for foreign tax already paid: If a foreign client’s country deducted tax, for example the US deducting 30% on certain payments, you can claim that amount back as a credit using Form 67. India’s Double Taxation Avoidance Agreements with various countries exist specifically to prevent the same income from being taxed twice.

Step 4: Understanding TDS

Many Indian clients are legally required to deduct tax before paying you. TDS, called Tax Deducted at Source, under Section 194J applies at 10% for professional and technical services.

This is not an additional tax. Think of it as tax paid early on your behalf. When you file your return at the end of the year, you claim full credit for whatever your clients deducted, and the tax authority adjusts it against your total tax liability.

One important habit to build: always check your Form 26AS and Annual Information Statement on the income tax portal before filing. These documents show exactly how much TDS the government has on record for you. If the figures do not match what your clients actually deducted, it can trigger a tax notice. Catching mismatches early saves a lot of trouble later.

Step 5: Pay Advance Tax on Time

If your tax liability exceeds ₹10,000, you must pay advance tax rather than settling it all at year-end. Salaried employees rarely deal with this because their employer handles most of it through TDS. For freelancers, TDS from clients may cover part of your liability, but it rarely covers all of it, especially if you have multiple income sources or your earnings grow through the year. You need to pay the remaining tax in advance. Missing it leads to interest charges under Sections 234B and 234C.

- If you opt for Section 44ADA and have no other major income source, you can pay 100% of your advance tax in a single installment on or before 15 March of the financial year.

- If you file under regular provisions (ITR-3) or have other income like salary, rent, or capital gains alongside your freelance work, you must follow the standard four-installment schedule, with payments due in June, September, December, and March.

Late or underpaying triggers automatic interest. Estimate your annual income early and set funds aside quarterly, not scrambling in March.

Step 6: File the Correct ITR Form

Choosing the right form matters as much as calculating the right tax.

- ITR-4 (Sugam): Use this if you are opting for presumptive taxation under Section 44ADA and have no complications like capital gains or foreign assets.

- ITR-3: Use this if you are calculating actual profits, have capital gains, own more than one house property, have foreign income or assets, or do not qualify for the presumptive scheme.

The filing process typically involves logging into the income tax e-filing portal, checking your AIS and TIS to confirm what income the department already has on record, filling in your business or professional income details, submitting Form 10-IEA if you are switching between the old and new regimes, and completing Aadhaar OTP verification to make your filing valid.

Do You Need a Tax Consultant?

Freelancer income tax in India involves several moving parts: choosing the right regime, picking between presumptive and actual taxation, tracking TDS, managing advance tax deadlines, and handling foreign income rules. For many freelancers, especially those just starting out with a single income source and straightforward earnings, filing independently is entirely manageable once you understand the basics.

However, a small mistake, like missing an advance tax installment, filing the wrong ITR form, or misreporting foreign income, can lead to penalties that cost more than professional help would have. This is where a tax consultant becomes valuable.

A good tax consultant does more than just file your return. They help you decide between the old and new regime based on your actual numbers, advise on whether Section 44ADA genuinely benefits you, and make sure your TDS credits and foreign income are reported correctly. For freelancers juggling multiple clients, international payments, or growing income, reliable tax consulting services free up time and significantly reduce the risk of costly errors.

If your income is growing, your client base is expanding internationally, or you are simply unsure about any step in the process, investing in tax consulting services is a practical decision rather than an unnecessary expense.

Frequently Asked Questions (FAQs)

Q1. Do freelancers need to pay income tax in India?

Yes. Any freelancer earning above the basic exemption limit is required to pay income tax in India. Freelance income is treated as income from business or profession, which means the same tax slabs and filing rules apply. New tax regime: ₹4 lakh exemption limit, zero tax up to ₹12 lakh with Section 87A rebate.

Q2. Which ITR form should a freelancer file?

Freelancers opting for presumptive taxation under Section 44ADA should file ITR-4. Those calculating actual profits, earning from foreign clients, or having capital gains alongside freelance income should file ITR-3. Filing the wrong form is a common mistake and can lead to a defective return notice from the tax department.

Q3. What is Section 44ADA and who can use it?

Section 44ADA is a presumptive taxation scheme that allows specified professionals to declare 50% of their gross receipts as taxable profit, without maintaining detailed books of accounts. It is available to freelancers in fields like engineering, legal, medical, architecture, technical consultancy, and interior decoration, provided their annual gross receipts do not exceed ₹50 lakh, or ₹75 lakh if less than 5% of receipts are in cash.

Q4. Is freelance income from foreign clients taxable in India?

Yes. If you are a tax resident of India, your income from foreign clients is fully taxable here regardless of which country the client is based in or which platform you used to receive payment. You must convert the amount to INR using your bank’s exchange rate on the date of receipt and report the full amount before any platform deductions. If tax was already deducted in the foreign country, you can claim relief under India’s Double Taxation Avoidance Agreements using Form 67.

Disclaimer: This article is intended for informational purposes only and does not constitute tax advice. Tax laws and deadlines are subject to change. Please consult a qualified tax consultant before making any filing decisions.